Lower Risk Guidelines for Online Wagering (Analysis Document)

Author

Rob Heirene

Published

June 3, 2025

Study pre-registration: https://osf.io/bx43k

Load Required Packages

Load in packages using groundhog to ensure consistency of the versions used here:

Show code

# Install and load the groundhog package to ensure consistency of the package versions used here:# install.packages("groundhog") # Installlibrary(groundhog) # Load# List desired packages:packages <-c('tidyverse', # Clean, organise, and visualise data'haven',# read spsss files"readxl", # load Excel files"survey", # weight study data"weights", # Weighted statistics "wCorr", # Weighted correlations (https://cran.r-project.org/web/packages/wCorr/wCorr.pdf)'kableExtra', # Make tables'formattable', # Add visualisations to tables'gt', # Alternative table options'gtExtras', # Add colours to gt tables'gtsummary', # Create summary tables'scales', # Allows for the removal of scientific notation in axis labels'plotly', # Add interactive elements to figures'htmlwidgets', # Make plotly plots HTML format'ggrain', # Make rain cloud plots'waffle', # make waffle plots for proportions'networkD3', # Make Sankey plots to show relationships'patchwork', # Join plots in multipanel layouts'pwr', # Check statistical power'car', # Perform ANCOVA stats tests'rstatix', # Perform ANCOVA stats tests'ggpubr', # Plots for linearity checks 'broom', # Print summaries of statistical test outputs'psych', # get detailed summary figures to Supplement statistical tests'sysfonts', # Special fonts for figures'showtext', # Special fonts for figures'ggstatsplot', # Plots with statistical outputs'janitor', # Make column names consistent format'caret', # Compute model performance indices'sessioninfo', # Detailed session info for reproducibility"osfr","readxl","googlesheets4",# Access data from Google sheets"Gmisc", # Produce prisma flow diagram'grid', # Produce prisma flow diagram"glue", # Produce prisma flow diagram"httpuv", # supports access to Google sheets"irr", # Compute interrater reliability stats"apa", # print test results in apa format"apaTables", # print test results in apa format"ggh4x", # truncate graph axis lines"remotes","misty", # read sav files"truncnorm", # Generate normally distributed data with limits"ggplot2","readr", # Load data'fmsb', # Compute NagelkerkeR2"performance", # Check model assumptions"see",# supports above package"robustbase", # Robust linear models"pscl", # Zero inflation model"cutpointr", # AUC/ROC"bestglm"# subset of limits modelling)# Load desired package with versions specific to project start date:groundhog.library(packages, "2025-02-28")

Setup Presentation & Graph Specifications

Set up a standard theme for plots/data visualisations:

Show code

# Load new font for figures/graphsfont_add_google("Poppins")font_add_google("Reem Kufi", "Reem Kufi")font_add_google("Share Tech Mono", "techmono")windowsFonts(`Segoe UI`=windowsFont('Segoe UI'))showtext_auto()showtext_auto(enable =TRUE)# Save new theme for figures/graphs.This will determine the layout, presentation, font type and font size used in all data visualisations presented here:plot_theme<-theme_classic() +theme(text=element_text(family="Poppins"),plot.title =element_text(hjust =0.5, size =16),plot.subtitle =element_text(hjust =0.5, size =13),axis.text =element_text(size =10),axis.title =element_text(size =12),plot.caption =element_text(size =12),legend.title=element_text(size=12), legend.text=element_text(size=10) )

Load Data

Load in master data set containing all customer details (code hidden):

Process the data for analysis by removing individuals who didn`t pass the attention checks and those who did not complete the survey:

Show code

master_dataset <- master_dataset_initial %>%as_tibble() %>%filter(SURVEY_STATUS_PGSI =="Complete") %>%filter(PAS_6M_BET_FREQ_DAYS !=0) %>%# Remove anybody who didn't bet in the window of interestfilter( (ATTENTION_CHECK_1 =="PASSED"|is.na(ATTENTION_CHECK_1)) & (ATTENTION_CHECK_2 =="PASSED"|is.na(ATTENTION_CHECK_2)) ) %>%mutate(GHM_OVER_PRIORITISE =as.numeric(GHM_OVER_PRIORITISE),GHM_STRAIN =as.numeric(GHM_STRAIN),GHM_SEVERE =as.numeric(GHM_SEVERE) ) %>%# Enforce the order of factors so that they present properly in tables and graphs:mutate(PGSI_CATEGORY =factor(PGSI_CATEGORY, levels =c('No risk','Low risk','Moderate risk','High risk')))# colnames(master_dataset)

Analyses - Survey

Recruitment

Provide some key figures for the participant section in the methods.

All behavioural indicator variables have been previously created in a separate script. For the interest of transparency, we will summarise all of these variables here:

Show code

master_dataset %>%select(PAS_6M_MONTHLY_BET_FREQ_DAYS, PAS_6M_MONTHLY_SPEND, PAS_6M_N_ACTIVITIES, PERCENT_MON_INCOME_SPENT_MONTHLY_PAS_6M, PAS_6M_MONTHLY_DEPOSIT_FREQ, PAS_6M_MONTHLY_DEPOSIT_AMOUNT, PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M, GAM_ACCOUNTS # Including this account, how many online gambling accounts have you used in the past 12 months? ) %>%gt_plt_summary()

.

1647 rows x 8 cols

Column

Plot Overview

Missing

Mean

Median

SD

PAS_6M_MONTHLY_BET_FREQ_DAYS

0.0%

9.1

6.6

8.2

PAS_6M_MONTHLY_SPEND

0.0%

8,040.2

540.8

24,719.4

PAS_6M_N_ACTIVITIES

0.0%

5.1

4.0

3.8

PERCENT_MON_INCOME_SPENT_MONTHLY_PAS_6M

35.9%

67.2

4.7

202.9

PAS_6M_MONTHLY_DEPOSIT_FREQ

0.0%

26.8

4.0

60.6

PAS_6M_MONTHLY_DEPOSIT_AMOUNT

0.0%

2,931.7

184.2

7,413.6

PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M

35.9%

25.2

1.6

70.7

GAM_ACCOUNTS

2, 3, 1, 5+ and 4

0.0%

—

—

—

We do, however, need to recode the ‘number of accounts’ variable to be consistent with our preregistration by converting it to a numeric format and replacing the ‘5 or more’ category with the value 5. We also need to limit people’s percentage of income deposited values to 100% to be consistent with our pre-registration and previous literature. Note that we will not look to restrict the percentage of income spent on gambling as it is theoretically possible for people to spend more than their total income if they are turning over winnings. By contrast, it would be unlikely for somebody to be able to deposit more than 100% of their income, unless they were reinvesting substantial winnings already withdrawn.

Let’s check how many people deposited more than 100% of their stated income:

74 people. Okay, let’s restrict these values to 100% when we recode the demographic control variables below.

Recode Other gambling control variables

Show code

master_dataset <- master_dataset %>%# Create Variable with dichotomous response options for engaging with gambling:mutate(Engages_in_other_forms =ifelse(GAM_ACTIVITIES !="None of the above"&!is.na(GAM_ACTIVITIES), TRUE, FALSE)) %>%# Convert number of gambling accounts to numeric:mutate(GAM_ACCOUNTS_NUM =case_when(GAM_ACCOUNTS =="1"~1, GAM_ACCOUNTS =="2"~2, GAM_ACCOUNTS =="3"~3, GAM_ACCOUNTS =="4"~4, GAM_ACCOUNTS =="5+"~5 )) # count(GAM_ACCOUNTS, GAM_ACCOUNTS_NUM) # Check the coding

Recode Demographic Control Variables

Some work will be needed to code the demographic control variables listed in the preregistration:

Age: A continuous variable provided by the sites. [No recoding required]

Gender: A categorical variable with 3 groups: male, female, and unknown. The male value will be set as the reference value. [No recoding required]

Employment status: Participants in the survey are asked to state their current employment status. Consistent with the approach used by Brosowki et al. (2015), we will simply recode all categories so that each person is assigned one of two labels: “Employed” (which will include the options for retirement and a full-time student) or “Unemployed” (which will also include being principally engaged in domestic duties), with the former being the reference value. [Recoded in code chunk below]

Education level: Participants in the survey were asked to state their highest level of educational achievement, selecting from 8 possible options of increasing obtainment. We will convert these categories into numerical values, with lower values indicating less education and vice versa. [Recoded in code chunk below]

Show code

# Education level:master_dataset$EDUCATION <-factor(master_dataset$EDUCATION, levels =rev(c("Doctoral degree","Master's degree","Graduate diploma or graduate level certificate","Bachelor's degree","Advanced diploma/diploma","Certificate III/IV","Year 12","Year 11 or below (includes Certificate I/II/n)")))# levels(master_dataset$EDUCATION) # Check# Define the numeric levels:education_levels <-c("Year 11 or below (includes Certificate I/II/n)"=1,"Year 12"=2,"Certificate III/IV"=3,"Advanced diploma/diploma"=4,"Bachelor's degree"=5,"Graduate diploma or graduate level certificate"=6,"Master's degree"=7,"Doctoral degree"=8)# Convert to numeric:master_dataset$EDUCATION_NUM <-as.numeric(factor(master_dataset$EDUCATION, levels =names(education_levels), labels = education_levels))# Add missing values:# First check median value of each PgSI group# master_dataset %>%# group_by(PGSI_CATEGORY) %>%# summarise(median(EDUCATION_NUM, na.rm = TRUE))# Okay, they're all the same, which is probably a good thing.# Now we come to impute group-specific median value for missing responses:master_dataset_w_demographics <- master_dataset %>%group_by(PGSI_CATEGORY) %>%mutate(EDUCATION_NUM =if_else(is.na(EDUCATION_NUM),median(EDUCATION_NUM, na.rm =TRUE), EDUCATION_NUM ) ) %>%ungroup()# master_dataset_w_demographics%>%# count(EDUCATION_NUM)# Employment status:# Check levels:# master_dataset %>%# count(EMPLOYMENT)master_dataset_w_demographics <- master_dataset_w_demographics %>%mutate(EMPLOYMENT_RECODED =case_when( EMPLOYMENT %in%c("Employed full time", "Employed full time,Employed part time or casual", "Employed full time,Full-time student", "Employed full time,Retired", "Employed part time or casual", "Employed part time or casual,Full-time student", "Employed part time or casual,Retired","Employed part time or casual,Principally engaged in domestic duties", "Full-time student", "Retired","Not currently employed,Retired") ~"Employed",# Categories for "Unemployed" EMPLOYMENT %in%c("Employed part time or casual,Not currently employed", "Not currently employed", "Not currently employed,Principally engaged in domestic duties", "Principally engaged in domestic duties") ~"Unemployed",is.na(EMPLOYMENT) ~"Unknown",# Default case to handle any unforeseen values (will work with any new data then!):TRUE~"Other" ) ) %>%# Per our preregistration, cap percentage of income deposited to 100%mutate(PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M =case_when(PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M >100~100,TRUE~ PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M))# master_dataset_w_demographics %>%# count(EMPLOYMENT_RECODED, PGSI_CATEGORY)

Recode Outcome Variables

Below is the description of the two outcome measures we will be using in this study taken from our preregistration.

PGSI harm index: Consistent with previous investigations of low-risk guidelines (e.g., Dowling et al., 2021), we will focus on the seven items relating to gambling harms within the PGSI (i.e., feeling guilty, losing more than one can afford, recognition of the problem, health problems, financial problems, criticism from others, and borrowing money). For each of these items, the participant will be scored as 0, representing a response of “never” on the PGSI, or 1, representing a score of “sometimes”, “most of the time”, or “almost always”. A score of 2 or more on these 7 items will be used to classify a participant as harmed.

For the purposes of accurate recoding, let’s list out the items in the PGSI and code them as to whether they are relevant or not:

Have you bet more than you could really afford to lose? [losing more than one can afford]

Have you needed to gamble with larger amounts to get the same feeling of excitement? [not scored]

When you gambled, did you go back another day to try to win back the money you lost? [not scored]

Have you borrowed money or sold anything to get money to gamble? [borrowing money]

Have you felt you might have a problem with gambling? [recognition of the problem]

Has gambling caused you any health problems, including stress or anxiety? [physical health problems]

Have people criticised your betting or told you that you had a gambling problem, regardless of whether or not you thought it was true? [criticism from others]

Has your gambling caused any financial problems for you or your household? [financial problems]

Have you felt guilty about the way you gamble or what happens when you gamble? [feeling guilty]

GHM harm index: For this index, we will use the Gambling Harm Measure (O’Neil et al., 2021), a 16-item scale measuring the impact of gambling across six life domains (financial, psychological, relationship, physical health, work/study, and legal). Dichotomous responses (yes/no) are provided to all questions which are asked in relation to the last 12 months (e.g., In the last 12 MONTHS, have you experienced any serious relationship consequences because of your gambling? For example, have you lost friends or family; or experienced separation or divorce; or engaged in physically violent arguments?). Questions are asked in a graded manner with three questions for each domain, the first asking about prioritising gambling over an activity/responsibility, the second asking about strains or pressures caused by gambling in that domain, and the third asking about serious consequences of gambling in that domain (the third level of questioning is only presented to participants if they say they have experienced harm at the strain/pressure level [2nd question] in that domain). For example, see below the three questions for financial harm:

In the last 12 MONTHS, has gambling led you to prioritise or put gambling ahead of other important financial expenditures? For example, has your gambling reduced money available for household or other important expenses?

In the last 12 MONTHS, have you experienced any financial pressures due to your gambling? For example, have you been building up debt; or found it hard to pay bills; or had to borrow money; or taken on extra work to finance gambling?

[Asked if participant responded “yes” to above question] In the last 12 MONTHS, have you experienced any serious financial consequences because of your gambling? For example, have you had to sell important assets; or been unable to pay rent or meet essential daily expenses; or had utilities disconnected; or lost your home; or filed for bankruptcy?

For this index, any participant who responds “yes” to a question at the second level of any domain (i.e., strain/pressure level of harm) will be classed as harmed. Note that the legal domain only has one question (”In the last 12 MONTHS, have you done anything illegal due to your gambling? For example, have you stolen money or valuables, or committed fraud or embezzlement, etc.?“). A positive response to this question will also result in a participant being classed as harmed.

Using the above descriptions for guidance, let’s now recode the outcome variables:

Show code

master_dataset_recoded <- master_dataset_w_demographics %>%rowwise() %>%mutate(across(c(PGSI_Q1, PGSI_Q2, PGSI_Q3, PGSI_Q4, PGSI_Q5, PGSI_Q6, PGSI_Q7, PGSI_Q8, PGSI_Q9), ~case_when( . =="Never"~"0", . =="Sometimes"~"1", . =="Most of the Time"~"1", . =="Always"~"1"))) %>%mutate(across(c(PGSI_Q1, # Convert PGSI questions from character to numeric PGSI_Q2, PGSI_Q3, PGSI_Q4, PGSI_Q5, PGSI_Q6, PGSI_Q7, PGSI_Q8, PGSI_Q9), as.numeric)) %>%mutate(PGSI_COUNT_STATUS =sum(PGSI_Q1, # PGSI_Q4, # PGSI_Q5, # PGSI_Q6, # PGSI_Q7, # PGSI_Q8, # PGSI_Q9, #na.rm =TRUE)) %>%mutate(PGSI_STATUS =case_when(PGSI_COUNT_STATUS <2~"No harm", PGSI_COUNT_STATUS >=2~"Harm",is.na(PGSI_COUNT_STATUS) ~NA )) %>%# Do some checks to see if coding worked correctly:# count(PGSI_COUNT_STATUS, PGSI_STATUS)# count(PGSI_STATUS)# GHM outcome measure:mutate(GHM_L1 =if_else(GHM_L1 ==3,1, GHM_L1)) %>%mutate(GHM_COUNT_STATUS =if_else(!is.na(GHM_F2) &!is.na(GHM_P2) &!is.na(GHM_R2) &!is.na(GHM_PH2) &!is.na(GHM_WS2) &!is.na(GHM_L1), # Only compute this value if all scores are present (i.e., someone completed the measure)sum( GHM_F2, # Financial GHM_P2, # Psychological health GHM_R2, # Relationships GHM_PH2, # Physical health GHM_WS2, # Work or study GHM_L1, # Legalna.rm =TRUE ),NA# Set to NA if any values are missing )) %>%mutate(GHM_STATUS =case_when(GHM_COUNT_STATUS ==0~"No harm", GHM_COUNT_STATUS >0~"Harm",is.na(GHM_COUNT_STATUS) ~NA )) %>%ungroup() # Remove rowise grouping!# Do some checks to see if coding worked correctly:# count(GHM_COUNT_STATUS, GHM_STATUS)# select(GHM_F2,# GHM_P2,# GHM_R2,# GHM_PH2,# GHM_WS2,# GHM_L1,# GHM_COUNT_STATUS,# GHM_STATUS) %>%# print(n=1000)# master_dataset_recoded %>%# count(GHM_STATUS)

Weighting

Many of the results presented from now are weighted outcomes. Let’s create the data frame required for weighting:

Phase 2: Identifying Optimal Limits for Behavioural Indicators

Now we are going to see if we can identify optimal limit/cut off/thresholds for each of the behavioural indicators against both the PGSI and the GHM harm index.

We’re going to need to extract a lot of outcomes from this process and summarise them into a table. Hence, we will create some functions to help with this process here:

Show code

# Youden optimisation function: # Start by defining key variables/inputs for the cutpoint function:summarize_auc_results_youden <-function(data, predictor_var, pgsi_status, GHM_status, pos_class ="Harm", neg_class ="No harm", boot_runs =2000) {# Calculate Threshold value & AUC results for PGSI: youden_cutpoint_pgsi <-cutpointr(data, {{ predictor_var }}, {{ pgsi_status }},pos_class = pos_class, direction =">=",neg_class = neg_class,method = maximize_boot_metric, metric = youden,boot_runs = boot_runs, na.rm =TRUE)# Calculate CI's for this: pgsi_auc_cis <-boot_ci(youden_cutpoint_pgsi, AUC, in_bag =TRUE, alpha =0.05) %>%select(values) %>%t() %>%as_tibble() %>%mutate(across(everything(), ~round(as.numeric(.), 3))) %>%unite("95%CIs_PGSI", V1, V2, sep =", ")# Join these results so far: auc_results_pgsi <- youden_cutpoint_pgsi %>%select(predictor,optimal_cutpoint_PGSI = optimal_cutpoint,AUC_PGSI = AUC,sensitivity_PGSI = sensitivity,specificity_PGSI = specificity, acc_PGSI = acc) %>%mutate(Metric_maximised ="Youden")# Calculate Threshold value & AUC results for GHM: youden_cutpoint_ghm <-cutpointr(data, {{ predictor_var }}, {{ GHM_status }},pos_class = pos_class, neg_class = neg_class,direction =">=",method = maximize_boot_metric, metric = youden,boot_runs = boot_runs, na.rm =TRUE)# Calculate CI's for this: GHM_auc_cis <-boot_ci(youden_cutpoint_ghm, AUC, in_bag =TRUE, alpha =0.05) %>%select(values) %>%t() %>%as_tibble() %>%mutate(across(everything(), ~round(as.numeric(.),3))) %>%unite("95%CIs_GHM", V1, V2, sep =", ")# Join these results so far: auc_results_ghm <- youden_cutpoint_ghm %>%select(optimal_cutpoint_GHM = optimal_cutpoint,AUC_GHM = AUC,sensitivity_GHM = sensitivity,specificity_GHM = specificity, acc_GHM = acc)# Combine all results into a single summary table: auc_summary <-bind_cols(auc_results_pgsi, pgsi_auc_cis, auc_results_ghm, GHM_auc_cis)return(auc_summary)}# I use the below code to check we get similar results for the first variable of interest (they won't be identical because of bootstrapping) and indeed we do. # Youden_cutpoint_PAS_6M_MONTHLY_BET_FREQ_DAYS_PGSI<- cutpointr(master_dataset_recoded, PAS_6M_MONTHLY_BET_FREQ_DAYS, PGSI_STATUS, pos_class = "Harm", neg_class = "No harm", method = maximize_boot_metric, metric = youden, boot_runs = 1000)# # Youden_cutpoint_PAS_6M_MONTHLY_BET_FREQ_DAYS_PGSI# # PAS_6M_MONTHLY_BET_FREQ_DAYS_PGSI_AUC_CIS_PGSI<- boot_ci(Youden_cutpoint_PAS_6M_MONTHLY_BET_FREQ_DAYS_PGSI, AUC, in_bag = TRUE, alpha = 0.05) # This should compute 95% CIs for AUC values# # # plot(Youden_cutpoint_PAS_6M_MONTHLY_BET_FREQ_DAYS_PGSI)# # Youden_cutpoint_PAS_6M_MONTHLY_BET_FREQ_DAYS_GHM<- cutpointr(master_dataset_recoded, PAS_6M_MONTHLY_BET_FREQ_DAYS, GHM_STATUS, pos_class = "Harm", neg_class = "No harm", method = maximize_boot_metric, metric = youden, boot_runs = 1000)# # PAS_6M_MONTHLY_BET_FREQ_DAYS_PGSI_AUC_CIS_GHM<-boot_ci(Youden_cutpoint_PAS_6M_MONTHLY_BET_FREQ_DAYS_GHM, AUC, in_bag = TRUE, alpha = 0.05) # This should compute 95% CIs for AUC values# # # plot(Youden_cutpoint_PAS_6M_MONTHLY_BET_FREQ_DAYS_GHM)# Sensitivity optimisation function: # Start by defining key variables/inputs for the cutpoint function, This time noting that we are maximising sensitivity and constraining specificity to a minimum of 0.5:summarize_auc_results_max_sensitivity <-function(data, predictor_var, pgsi_status, GHM_status, pos_class ="Harm", neg_class ="No harm", boot_runs =2000) {# Calculate Threshold value & AUC results for PGSI: youden_cutpoint_pgsi <-cutpointr(data, {{ predictor_var }}, {{ pgsi_status }},pos_class = pos_class,neg_class = neg_class,direction =">=",method = maximize_boot_metric, metric = sens_constrain,constrain_metric = specificity, min_constrain =0.5,boot_runs = boot_runs,na.rm =TRUE)# Calculate CI's for this: pgsi_auc_cis <-boot_ci(youden_cutpoint_pgsi, AUC, in_bag =TRUE, alpha =0.05) %>%select(values) %>%t() %>%as_tibble() %>%mutate(across(everything(), ~round(as.numeric(.),3))) %>%unite("95%CIs_PGSI", V1, V2, sep =", ")# Join these results so far: auc_results_pgsi <- youden_cutpoint_pgsi %>%select(predictor,optimal_cutpoint_PGSI = optimal_cutpoint,AUC_PGSI = AUC,sensitivity_PGSI = sensitivity,specificity_PGSI = specificity, acc_PGSI = acc) %>%mutate(Metric_maximised ="Sensitivity")# Calculate Threshold value & AUC results for GHM: youden_cutpoint_ghm <-cutpointr(data, {{ predictor_var }}, {{ GHM_status }},pos_class = pos_class,neg_class = neg_class,direction =">=",method = maximize_boot_metric, metric = sens_constrain,constrain_metric = specificity,min_constrain =0.5,boot_runs = boot_runs, na.rm =TRUE)# Calculate CI's for this: GHM_auc_cis <-boot_ci(youden_cutpoint_ghm, AUC, in_bag =TRUE, alpha =0.05) %>%select(values) %>%t() %>%as_tibble() %>%mutate(across(everything(), ~round(as.numeric(.),3))) %>%unite("95%CIs_GHM", V1, V2, sep =", ")# Join these results so far: auc_results_ghm <- youden_cutpoint_ghm %>%select(optimal_cutpoint_GHM = optimal_cutpoint,AUC_GHM = AUC,sensitivity_GHM = sensitivity,specificity_GHM = specificity, acc_GHM = acc)# Combine all results into a single summary table: auc_summary <-bind_cols(auc_results_pgsi, pgsi_auc_cis, auc_results_ghm, GHM_auc_cis)return(auc_summary)}# Specificity optimisation function: # Start by defining key variables/inputs for the cutpoint function, This time noting that we are maximising Specificity and constraining Sensitivity to a minimum of 0.5:summarize_auc_results_max_specificity <-function(data, predictor_var, pgsi_status, GHM_status, pos_class ="Harm", neg_class ="No harm", boot_runs =2000) {# Calculate Threshold value & AUC results for PGSI: youden_cutpoint_pgsi <-cutpointr(data, {{ predictor_var }}, {{ pgsi_status }},pos_class = pos_class,neg_class = neg_class,direction =">=",method = maximize_boot_metric,metric = spec_constrain,constrain_metric = sensitivity,min_constrain =0.5,boot_runs = boot_runs, na.rm =TRUE)# Calculate CI's for this: pgsi_auc_cis <-boot_ci(youden_cutpoint_pgsi, AUC, in_bag =TRUE, alpha =0.05) %>%select(values) %>%t() %>%as_tibble() %>%mutate(across(everything(), ~round(as.numeric(.),3))) %>%unite("95%CIs_PGSI", V1, V2, sep =", ")# Join these results so far: auc_results_pgsi <- youden_cutpoint_pgsi %>%select(predictor, method,optimal_cutpoint_PGSI = optimal_cutpoint,AUC_PGSI = AUC,sensitivity_PGSI = sensitivity,specificity_PGSI = specificity, acc_PGSI = acc) %>%mutate(Metric_maximised ="Specificity")# Calculate Threshold value & AUC results for GHM: youden_cutpoint_ghm <-cutpointr(data, {{ predictor_var }}, {{ GHM_status }},pos_class = pos_class, neg_class = neg_class,direction =">=",method = maximize_boot_metric,metric = spec_constrain,constrain_metric = sensitivity,min_constrain =0.5,boot_runs = boot_runs, na.rm =TRUE)# Calculate CI's for this: GHM_auc_cis <-boot_ci(youden_cutpoint_ghm, AUC, in_bag =TRUE, alpha =0.05) %>%select(values) %>%t() %>%as_tibble() %>%mutate(across(everything(), ~round(as.numeric(.),3))) %>%unite("95%CIs_GHM", V1, V2, sep =", ")# Join these results so far: auc_results_ghm <- youden_cutpoint_ghm %>%select(optimal_cutpoint_GHM = optimal_cutpoint,AUC_GHM = AUC,sensitivity_GHM = sensitivity,specificity_GHM = specificity, acc_GHM = acc)# Combine all results into a single summary table: auc_summary <-bind_cols(auc_results_pgsi, pgsi_auc_cis, auc_results_ghm, GHM_auc_cis)return(auc_summary)}

Because of the extensive bootstrapping required for the three approaches across eight different behavioural indicators, the code below takes quite a bit of time to run. Hence, it has been commented out to save time each time the script runs or document knits. The outcomes from the bootstrapping were saved to a data file which is loaded in at the end of this process.

# First join and then save all outcomes as a dataset for easy retrieval later on:# AUC_limit_outcome_data <- bind_rows(# PAS_6M_MONTHLY_BET_FREQ_DAYS_AUC_Youden,# PAS_6M_MONTHLY_BET_FREQ_DAYS_AUC_Sensitivity,# PAS_6M_MONTHLY_BET_FREQ_DAYS_AUC_Specificity,# PAS_6M_MONTHLY_SPEND_AUC_Youden,# PAS_6M_MONTHLY_SPEND_AUC_Sensitivity,# PAS_6M_MONTHLY_SPEND_AUC_Specificity,# PERCENT_MON_INCOME_SPENT_MONTHLY_PAS_6M_AUC_Youden,# PERCENT_MON_INCOME_SPENT_MONTHLY_PAS_6M_AUC_Sensitivity,# PERCENT_MON_INCOME_SPENT_MONTHLY_PAS_6M_AUC_Specificity,# PAS_6M_N_ACTIVITIES_AUC_Youden,# PAS_6M_N_ACTIVITIES_AUC_Sensitivity,# PAS_6M_N_ACTIVITIES_AUC_Specificity,# PAS_6M_MONTHLY_DEPOSIT_FREQ_AUC_Youden,# PAS_6M_MONTHLY_DEPOSIT_FREQ_AUC_Sensitivity,# PAS_6M_MONTHLY_DEPOSIT_FREQ_AUC_Specificity,# PAS_6M_MONTHLY_DEPOSIT_AMOUNT_AUC_Youden,# PAS_6M_MONTHLY_DEPOSIT_AMOUNT_AUC_Sensitivity,# PAS_6M_MONTHLY_DEPOSIT_AMOUNT_AUC_Specificity,# PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M_AUC_Youden,# PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M_AUC_Sensitivity,# PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M_AUC_Specificity,# GAM_ACCOUNTS_AUC_Youden,# GAM_ACCOUNTS_AUC_Sensitivity,# GAM_ACCOUNTS_AUC_Specificity# ) %>%# mutate_if(is.numeric, round, 3)# # write.csv(AUC_limit_outcome_data,# "R Data files/AUC_limit_outcome_data.csv",# row.names=FALSE)# Read in outcome data:AUC_limit_outcome_data<-read.csv("R Data files/AUC_limit_outcome_data.csv")# Table them:AUC_limit_outcome_data %>%gt() %>%tab_options(data_row.padding =px(1.5))%>%tab_header(title ="Supplemental Table 1. Performance metrics for all cut-off points for all behavioural indicators" )

Supplemental Table 1. Performance metrics for all cut-off points for all behavioural indicators

predictor

optimal_cutpoint_PGSI

AUC_PGSI

sensitivity_PGSI

specificity_PGSI

acc_PGSI

Metric_maximised

X95.CIs_PGSI

optimal_cutpoint_GHM

AUC_GHM

sensitivity_GHM

specificity_GHM

acc_GHM

X95.CIs_GHM

method

PAS_6M_MONTHLY_BET_FREQ_DAYS

9.051

0.560

0.443

0.646

0.536

Youden

0.533, 0.587

7.447

0.573

0.553

0.565

0.561

0.542, 0.604

NA

PAS_6M_MONTHLY_BET_FREQ_DAYS

5.681

0.560

0.579

0.507

0.546

Sensitivity

0.532, 0.587

6.285

0.573

0.587

0.510

0.533

0.542, 0.606

NA

PAS_6M_MONTHLY_BET_FREQ_DAYS

7.861

0.560

0.496

0.602

0.545

Specificity

0.533, 0.589

8.563

0.573

0.498

0.605

0.573

0.544, 0.603

maximize_boot_metric

PAS_6M_MONTHLY_SPEND

932.621

0.621

0.514

0.688

0.594

Youden

0.593, 0.648

899.123

0.648

0.602

0.649

0.635

0.619, 0.678

NA

PAS_6M_MONTHLY_SPEND

251.420

0.621

0.685

0.497

0.599

Sensitivity

0.594, 0.648

332.348

0.648

0.712

0.514

0.573

0.619, 0.679

NA

PAS_6M_MONTHLY_SPEND

1062.813

0.621

0.497

0.700

0.590

Specificity

0.594, 0.649

2108.328

0.648

0.494

0.737

0.665

0.619, 0.678

maximize_boot_metric

PERCENT_MON_INCOME_SPENT_MONTHLY

6.380

0.655

0.580

0.686

0.627

Youden

0.622, 0.688

8.923

0.667

0.635

0.692

0.674

0.631, 0.703

NA

PERCENT_MON_INCOME_SPENT_MONTHLY

2.119

0.655

0.711

0.511

0.621

Sensitivity

0.624, 0.69

2.749

0.667

0.739

0.508

0.582

0.633, 0.701

NA

PERCENT_MON_INCOME_SPENT_MONTHLY

11.280

0.655

0.499

0.745

0.609

Specificity

0.623, 0.687

16.941

0.667

0.501

0.751

0.671

0.632, 0.702

maximize_boot_metric

PAS_6M_N_ACTIVITIES

4.080

0.611

0.499

0.650

0.568

Youden

0.583, 0.637

4.580

0.618

0.551

0.623

0.601

0.588, 0.647

NA

PAS_6M_N_ACTIVITIES

4.100

0.611

0.499

0.650

0.568

Sensitivity

0.584, 0.638

4.820

0.618

0.551

0.623

0.601

0.59, 0.648

NA

PAS_6M_N_ACTIVITIES

4.680

0.611

0.499

0.650

0.568

Specificity

0.584, 0.639

5.000

0.618

0.551

0.623

0.601

0.588, 0.649

maximize_boot_metric

PAS_6M_MONTHLY_DEPOSIT_FREQ

3.806

0.651

0.623

0.630

0.626

Youden

0.624, 0.676

6.415

0.669

0.633

0.651

0.646

0.64, 0.698

NA

PAS_6M_MONTHLY_DEPOSIT_FREQ

1.776

0.651

0.719

0.513

0.625

Sensitivity

0.624, 0.677

2.299

0.669

0.754

0.504

0.578

0.64, 0.699

NA

PAS_6M_MONTHLY_DEPOSIT_FREQ

8.841

0.651

0.493

0.741

0.607

Specificity

0.626, 0.679

14.005

0.669

0.492

0.756

0.677

0.642, 0.699

maximize_boot_metric

PAS_6M_MONTHLY_DEPOSIT_AMOUNT

216.240

0.648

0.591

0.647

0.617

Youden

0.62, 0.674

259.193

0.667

0.676

0.634

0.647

0.638, 0.695

NA

PAS_6M_MONTHLY_DEPOSIT_AMOUNT

80.171

0.648

0.717

0.504

0.619

Sensitivity

0.621, 0.674

109.794

0.667

0.765

0.504

0.582

0.637, 0.696

NA

PAS_6M_MONTHLY_DEPOSIT_AMOUNT

471.498

0.648

0.496

0.725

0.601

Specificity

0.622, 0.674

904.495

0.667

0.494

0.742

0.668

0.637, 0.696

maximize_boot_metric

PERCENT_MON_INCOME_DEPOSIT_MONTHLY

2.129

0.691

0.604

0.709

0.651

Youden

0.66, 0.724

3.393

0.690

0.638

0.698

0.679

0.654, 0.724

NA

PERCENT_MON_INCOME_DEPOSIT_MONTHLY

0.652

0.691

0.766

0.502

0.647

Sensitivity

0.659, 0.724

0.925

0.690

0.786

0.506

0.595

0.656, 0.723

NA

PERCENT_MON_INCOME_DEPOSIT_MONTHLY

5.122

0.691

0.504

0.785

0.630

Specificity

0.66, 0.723

9.617

0.690

0.496

0.788

0.695

0.656, 0.723

maximize_boot_metric

GAM_ACCOUNTS_NUM

3.000

0.610

0.606

0.576

0.592

Youden

0.585, 0.636

3.240

0.612

0.375

0.764

0.647

0.581, 0.64

NA

GAM_ACCOUNTS_NUM

3.000

0.610

0.606

0.576

0.592

Sensitivity

0.583, 0.636

3.100

0.612

0.375

0.764

0.647

0.583, 0.641

NA

GAM_ACCOUNTS_NUM

3.000

0.610

0.606

0.576

0.592

Specificity

0.585, 0.637

3.000

0.612

0.633

0.526

0.558

0.581, 0.641

maximize_boot_metric

Find Optimal Limits

Isolate the optimal limits/cut-off values for PGSI and GHM classification based on our preregistered plan:

Show code

PGSI_optimal_limits <- AUC_limit_outcome_data %>%group_by(predictor) %>%filter(acc_PGSI ==max(acc_PGSI)) %>%slice(1) %>%mutate(AUC_with_CI_PGSI =paste0(round(AUC_PGSI, 3), " [", gsub(",", ",", gsub("\\[|\\]", "", X95.CIs_PGSI)), "]" ) ) %>%select(predictor, AUC_with_CI_PGSI, Metric_maximised, optimal_cutpoint_PGSI, acc_PGSI, sensitivity_PGSI, specificity_PGSI)GHM_optimal_limits <- AUC_limit_outcome_data %>%group_by(predictor) %>%filter(acc_GHM ==max(acc_GHM)) %>%slice(1) %>%mutate(AUC_with_CI_GHM =paste0(round(AUC_GHM, 3), " [", gsub(",", ",", gsub("\\[|\\]", "", X95.CIs_GHM)), "]" ) ) %>%select(predictor, AUC_with_CI_GHM, Metric_maximised, optimal_cutpoint_GHM, acc_GHM, sensitivity_GHM, specificity_GHM)optimal_limits<-bind_cols(PGSI_optimal_limits, GHM_optimal_limits) %>%rename(Predictor =1,'Metric maximised PGSI'= Metric_maximised...3,'Metric maximised GHM'= Metric_maximised...10) %>%select(-predictor...8) %>%mutate(Predictor =case_when(Predictor =="PERCENT_MON_INCOME_SPENT_MONTHLY"~"PERCENT_MON_INCOME_SPENT_MONTHLY_PAS_6M", Predictor =="PERCENT_MON_INCOME_DEPOSIT_MONTHLY"~"PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M",TRUE~ Predictor))# Sort order:predictor_order <-c("PAS_6M_MONTHLY_BET_FREQ_DAYS","PAS_6M_MONTHLY_SPEND","PERCENT_MON_INCOME_SPENT_MONTHLY_PAS_6M","PAS_6M_N_ACTIVITIES","PAS_6M_MONTHLY_DEPOSIT_FREQ","PAS_6M_MONTHLY_DEPOSIT_AMOUNT","PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M","GAM_ACCOUNTS_NUM")optimal_limits <- optimal_limits %>%mutate(Predictor =factor(Predictor, levels = predictor_order)) %>%arrange(Predictor) %>%mutate(optimal_cutpoint_PGSI =round(optimal_cutpoint_PGSI,2),optimal_cutpoint_GHM =round(optimal_cutpoint_GHM,2))# Make table:gt(optimal_limits) %>%tab_row_group(label ="Guidelines examined in previous studies", rows =5:8 ) %>%tab_row_group(label ="Online wagering specific guidelines not previously examined", rows =1:4 ) %>%#### Example from other table:cols_label(Predictor ="Behavioural indicator",AUC_with_CI_PGSI ="AUC [95% CIs]",'Metric maximised PGSI'="Metric maximised",optimal_cutpoint_PGSI ="Optimal cut point",acc_PGSI ="Accuracy",sensitivity_PGSI ="Sensitivity",specificity_PGSI ="Specificity",AUC_with_CI_GHM ="AUC [95% CIs]",'Metric maximised GHM'="Metric maximised",optimal_cutpoint_GHM ="Optimal cut point",acc_GHM ="Accuracy",sensitivity_GHM ="Sensitivity",specificity_GHM ="Specificity", ) %>%tab_options(data_row.padding =px(2.5)) %>%tab_header(title ="Table 2. Optimal limit values for low-risk guidelines for online wagering with classification performance metrics" ) %>%tab_footnote( "Note: PGSI = Problem Gambling Severity Index; GHM = Gambling Harm Measure; AUC = Area under the curve; CIs = 95% Confidence intervals. Metric maximised = the approach used to reach the limit with the highest accuracy value for each behavioural indicator." )

Table 2. Optimal limit values for low-risk guidelines for online wagering with classification performance metrics

Behavioural indicator

AUC [95% CIs]

Metric maximised

Optimal cut point

Accuracy

Sensitivity

Specificity

AUC [95% CIs]

Metric maximised

Optimal cut point

Accuracy

Sensitivity

Specificity

Online wagering specific guidelines not previously examined

PAS_6M_MONTHLY_BET_FREQ_DAYS

0.56 [0.532, 0.587]

Sensitivity

5.68

0.546

0.579

0.507

0.573 [0.544, 0.603]

Specificity

8.56

0.573

0.498

0.605

PAS_6M_MONTHLY_SPEND

0.621 [0.594, 0.648]

Sensitivity

251.42

0.599

0.685

0.497

0.648 [0.619, 0.678]

Specificity

2108.33

0.665

0.494

0.737

PERCENT_MON_INCOME_SPENT_MONTHLY_PAS_6M

0.655 [0.622, 0.688]

Youden

6.38

0.627

0.580

0.686

0.667 [0.631, 0.703]

Youden

8.92

0.674

0.635

0.692

PAS_6M_N_ACTIVITIES

0.611 [0.583, 0.637]

Youden

4.08

0.568

0.499

0.650

0.618 [0.588, 0.647]

Youden

4.58

0.601

0.551

0.623

Guidelines examined in previous studies

PAS_6M_MONTHLY_DEPOSIT_FREQ

0.651 [0.624, 0.676]

Youden

3.81

0.626

0.623

0.630

0.669 [0.642, 0.699]

Specificity

14.01

0.677

0.492

0.756

PAS_6M_MONTHLY_DEPOSIT_AMOUNT

0.648 [0.621, 0.674]

Sensitivity

80.17

0.619

0.717

0.504

0.667 [0.637, 0.696]

Specificity

904.50

0.668

0.494

0.742

PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M

0.691 [0.66, 0.724]

Youden

2.13

0.651

0.604

0.709

0.69 [0.656, 0.723]

Specificity

9.62

0.695

0.496

0.788

GAM_ACCOUNTS_NUM

0.61 [0.585, 0.636]

Youden

3.00

0.592

0.606

0.576

0.612 [0.581, 0.64]

Youden

3.24

0.647

0.375

0.764

Note: PGSI = Problem Gambling Severity Index; GHM = Gambling Harm Measure; AUC = Area under the curve; CIs = 95% Confidence intervals. Metric maximised = the approach used to reach the limit with the highest accuracy value for each behavioural indicator.

Interestingly, when using the PGSI, maximising either the Youden index or sensitivity led to the best accuracy, when using the GHM, maximising Youden or specificity was most effective.

Phase 3: Demographic-adjusted Predictive Ability of New Limits

Here we started focus on testing H2. From our pre-registration:

H2: Participants who surpass each of our newly derived low-risk limits for the eight different behavioural indicators in the six months preceding survey participation will have a greater odds of reporting the experience of harm than who do not surpass the limits after accounting for the impact of demographic factors (i.e., age, gender, employment status, and education level) on harm. Specifically, the odds ratios produced via logistic regression models[1] for each of the eight limits will be ≥1.10[2] and 95% confidence intervals for these values will not cross 1, both when assessing each limit in isolation [H2.1] and when all limits are included in one statistical model to adjust for their relative contributions to the experience of harm [H2.2]. [Limit evaluation: demographic and other limit adjusted ability of limit breaches to predict harm status]

[1]All logistic regression models used to test hypotheses will include age and gender as predictor variables to account for their impact on gambling harm.

[2] This value represents our minimum effect size of interest in this context. We view a 10% increased odds of harm resulting from passing a low-risk limit as the minimum amount for a guideline to have practical value in informing about and identifying at-risk play.

First, to do this we need to add some new variables to a data set that label whether somebody passed our new limits or not.

Let’s now add new variables which represent whether somebody passed or did not pass the limits for PGSI and GHM. We will make each of the optimal limits rounded to the nearest whole number so that they are more actionable and representative of what we would recommend. Let’s also create a variable that sums the total number of limits someone passes:

Next, perform logistic regressions to examine how well exceeding each limit predicts harm status, controlling for demographic variables. For each analysis, two models will be run: one for the PGSI and one for the GHM.

For each model, we will run a function to produce plots showing diagnostic checks and then table regression outcomes together for the PGSI and GHM models, exponentiating betas into odds ratios.

tbl_merge(tbls =list(tbl_weighted_lr_freq_new_limit_PGSI, tbl_weighted_lr_freq_new_limit_GHM),tab_spanner =c("**PGSI Status**", "**GHM Status**")) %>%as_gt() %>%tab_options(data_row.padding =px(1.5)) %>%tab_header(title ="New optimal gambling frequency limit for online wagering as a predictor of harm status (demographic-adjusted models)" )

New optimal gambling frequency limit for online wagering as a predictor of harm status (demographic-adjusted models)

Characteristic

PGSI Status

GHM Status

OR

95% CI

p-value

OR

95% CI

p-value

AGE

0.97

0.96, 0.98

<0.001

0.97

0.96, 0.98

<0.001

GENDER

Female

—

—

—

—

Male

1.74

1.22, 2.49

0.002

2.28

1.36, 3.81

0.002

Unknown

2.24

0.82, 6.12

0.12

2.32

0.71, 7.62

0.2

EMPLOYMENT_RECODED

Employed

—

—

—

—

Unemployed

1.38

0.77, 2.47

0.3

2.72

1.48, 4.99

0.001

Unknown

1.17

0.88, 1.56

0.3

0.98

0.69, 1.40

>0.9

EDUCATION_NUM

0.90

0.83, 0.97

0.007

0.97

0.89, 1.06

0.5

GAM_ACCOUNTS_NUM

1.36

1.23, 1.49

<0.001

1.34

1.20, 1.48

<0.001

Engages_in_other_forms

FALSE

—

—

—

—

TRUE

1.88

1.38, 2.56

<0.001

1.74

1.20, 2.52

0.004

NEW_LIMIT_PGSI_BET_FREQ

1.37

1.07, 1.74

0.012

Null deviance

2,283

1,787

Null df

1,646

1,579

AIC

2,103

1,647

BIC

2,154

1,699

Deviance

2,080

1,625

Residual df

1,637

1,570

No. Obs.

1,647

1,580

NEW_LIMIT_GHM_BET_FREQ

1.37

1.01, 1.85

0.046

Abbreviations: CI = Confidence Interval, OR = Odds Ratio

Calculate Nagelkerke’s R squared for the PGSI model:

# NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

The model accounts for 15.4854331% of variance in PGSI harm rates.

Calculate Nagelkerke’s R squared for the GHM model:

Show code

NagelkerkeR2_weighted_bet_freq_GHM<-NagelkerkeR2(weighted_lr_freq_new_limit_GHM) %>%as.data.frame() %>%print() # NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

N R2

1 1580 0.1437819

The model accounts for 14.3781926% of variance in PGSI harm rates.

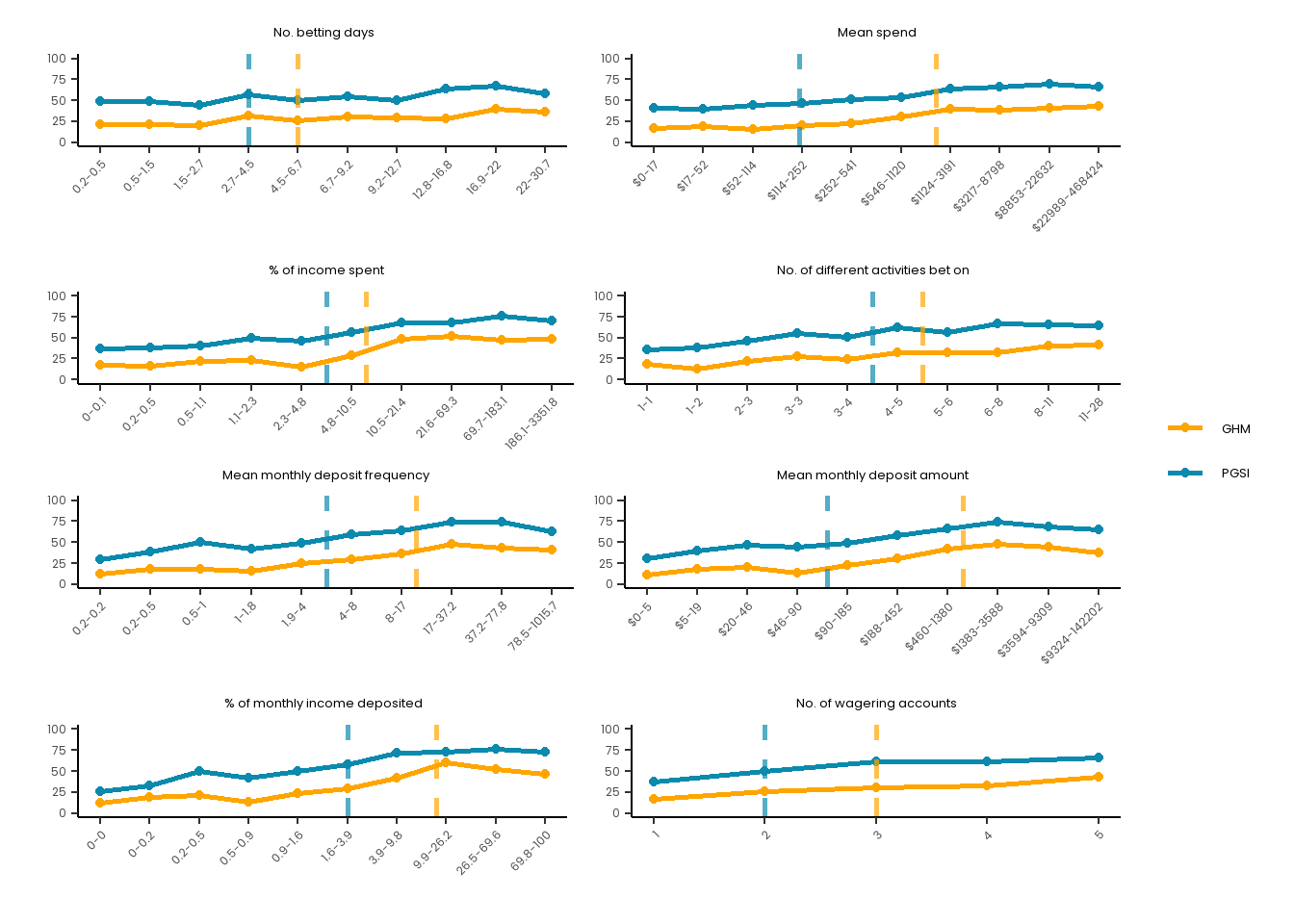

Risk Curve

Let’s plot some risk curves for the relationship between this predictor and the two outcomes. We didn’t pre-register this, but it’s purpose is solely for visual exploration/supplementation and will not be used for inference.

Show code

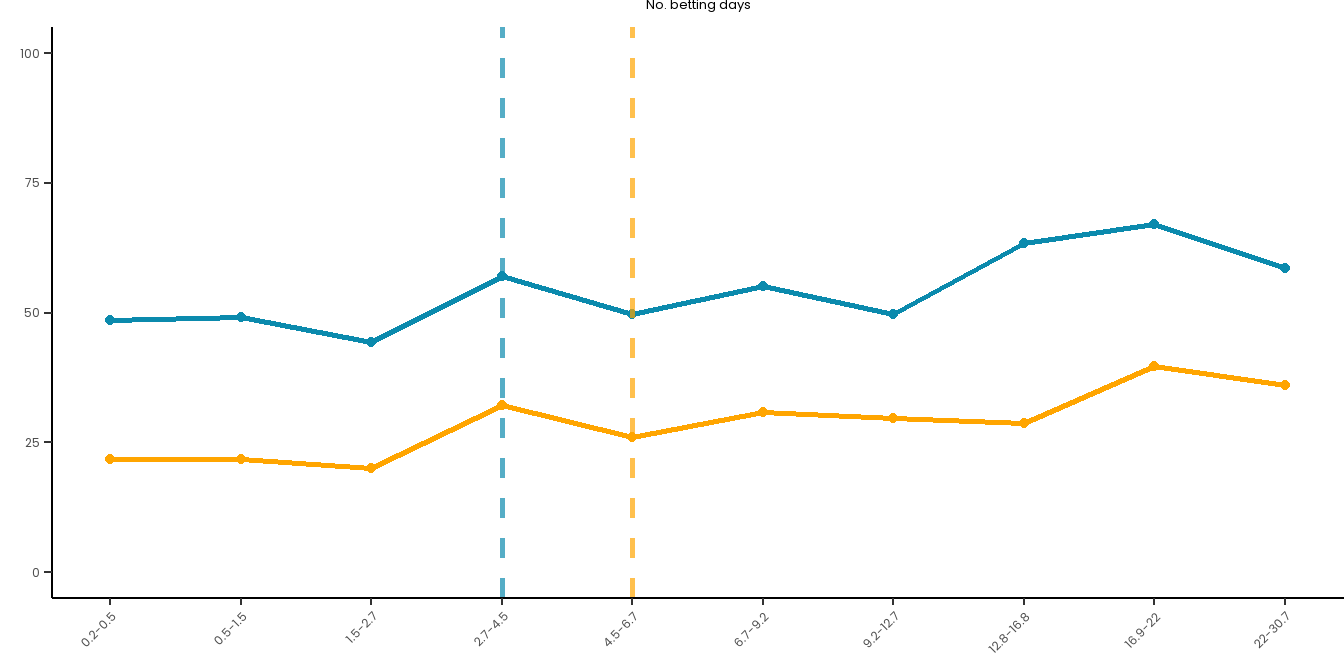

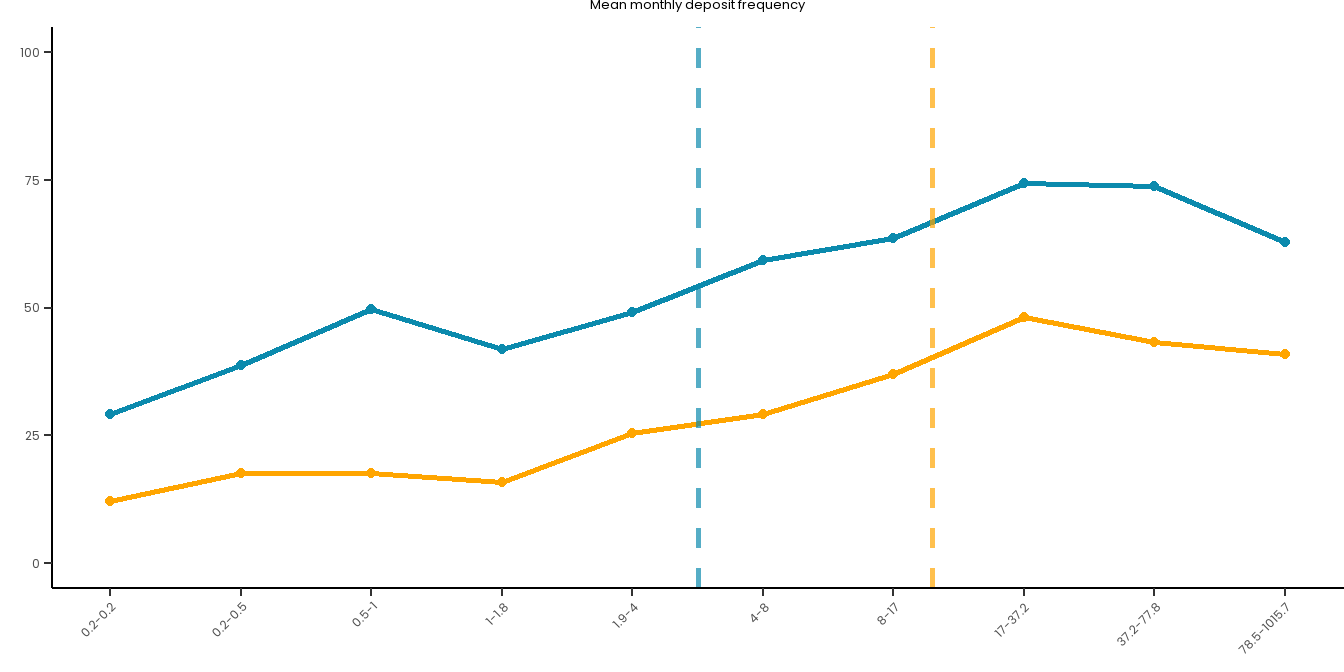

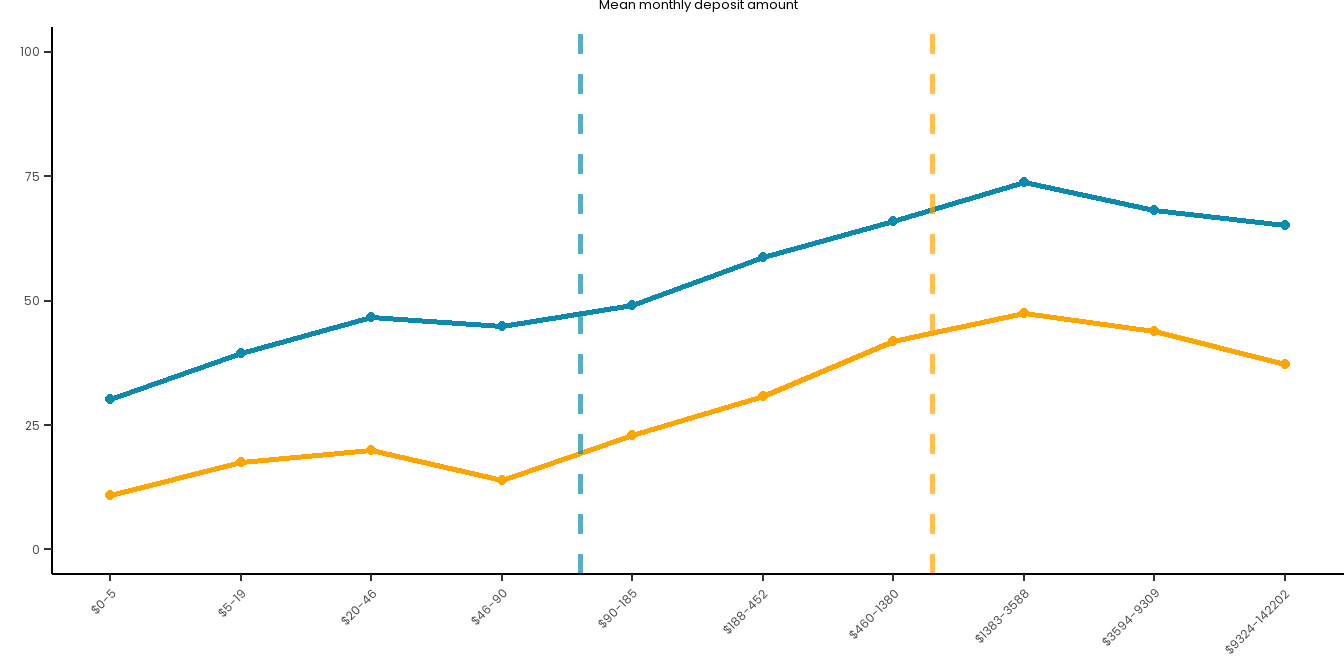

# Set up a good theme for these plots going forward:risk_curve_theme<-theme_classic() +theme(text =element_text(family ="Poppins"),plot.title =element_text(hjust =0.5, size =10, face ="plain"),plot.subtitle =element_text(hjust =0.5, size =13),axis.text.x =element_text(size =9, angle =45, hjust =1),axis.text.y =element_text(size =9),axis.title =element_text(size =10),plot.caption =element_text(size =12),legend.title =element_text(size =12), legend.text =element_text(size =10) ) # Create a summary dataset:summary_data <- master_dataset_recoded_w_new_limits %>%mutate(decile =ntile(PAS_6M_MONTHLY_BET_FREQ_DAYS, 10)) %>%group_by(decile) %>%summarise(PGSI_pct =sum(PGSI_STATUS ==1, na.rm =TRUE) /n() *100,GHM_pct =sum(GHM_STATUS ==1, na.rm =TRUE) /n() *100,min_val =min(PAS_6M_MONTHLY_BET_FREQ_DAYS, na.rm =TRUE),max_val =max(PAS_6M_MONTHLY_BET_FREQ_DAYS, na.rm =TRUE) ) %>%mutate(decile_label =paste(round(min_val, 1), round(max_val, 1), sep ="-"))long_data <- summary_data %>%pivot_longer(cols =c(PGSI_pct, GHM_pct),names_to ="HarmMeasure",values_to ="pct_harmed" ) %>%mutate(HarmMeasure =case_when(HarmMeasure =="PGSI_pct"~"PGSI", HarmMeasure =="GHM_pct"~"GHM"))# Plot both curves on the same plot for ease:combined_risk_curve_betting_freq <-ggplot(long_data, aes(x =as.numeric(decile), y = pct_harmed, color = HarmMeasure, group = HarmMeasure)) +geom_line(size =1) +geom_point() +scale_x_continuous(breaks =1:10, labels = summary_data$decile_label) +labs(title ="No. betting days",x ="",y ="") +ylim(0, 100) +# PGSI LIMIT:geom_vline(xintercept =4, linetype ="dashed", color ="#0B8AAD", size =1, alpha =0.7) +# GHM LIMIT:geom_vline(xintercept =5, linetype ="dashed", color ="orange", size =1, alpha =0.7) +scale_color_manual(name ="", values =c("PGSI"="#0B8AAD", "GHM"="orange")) + risk_curve_theme +theme(legend.position ="none",plot.margin =margin(0,0,-1,0)) combined_risk_curve_betting_freq

# NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

The model accounts for 17.8140946% of variance in PGSI harm rates.

Calculate Nagelkerke’s R squared for the GHM model:

Show code

NagelkerkeR2_weighted_spend_lr_GHM<-NagelkerkeR2(weighted_lr_spend_new_limit_GHM) %>%as.data.frame() %>%print() # NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

N R2

1 1580 0.1797802

The model accounts for 17.9780248% of variance in PGSI harm rates.

Risk Curve

Plot some risk curves for the relationship between this predictor and the two outcomes.

tbl_merge(tbls =list(tbl_weighted_lr_income_spent_new_limit_PGSI, tbl_weighted_lr_income_spent_new_limit_GHM),tab_spanner =c("**PGSI Status**", "**GHM Status**")) %>%as_gt() %>%tab_options(data_row.padding =px(1.5)) %>%tab_header(title ="New optimal percentage of income spent limit for online wagering as a predictor of harm status (demographic-adjusted models)" )

New optimal percentage of income spent limit for online wagering as a predictor of harm status (demographic-adjusted models)

Characteristic

PGSI Status

GHM Status

OR

95% CI

p-value

OR

95% CI

p-value

AGE

0.97

0.96, 0.98

<0.001

0.97

0.96, 0.98

<0.001

GENDER

Female

—

—

—

—

Male

1.73

1.07, 2.80

0.026

2.22

1.16, 4.24

0.015

Unknown

3.82

1.02, 14.3

0.047

1.71

0.44, 6.62

0.4

EMPLOYMENT_RECODED

Employed

—

—

—

—

Unemployed

1.06

0.52, 2.16

0.9

1.58

0.72, 3.46

0.3

EDUCATION_NUM

0.91

0.83, 1.0

0.037

0.99

0.90, 1.09

0.9

GAM_ACCOUNTS_NUM

1.34

1.19, 1.50

<0.001

1.38

1.20, 1.57

<0.001

Engages_in_other_forms

FALSE

—

—

—

—

TRUE

1.93

1.32, 2.82

<0.001

1.97

1.25, 3.10

0.003

NEW_LIMIT_PGSI_INCOME_SPENT

2.83

2.05, 3.93

<0.001

Null deviance

1,527

1,288

Null df

1,054

1,054

AIC

1,362

1,122

BIC

1,404

1,165

Deviance

1,342

1,103

Residual df

1,046

1,046

No. Obs.

1,055

1,055

NEW_LIMIT_GHM_INCOME_SPENT

4.49

3.11, 6.49

<0.001

Abbreviations: CI = Confidence Interval, OR = Odds Ratio

Calculate Nagelkerke’s R squared for the PGSI model:

# NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

The model accounts for 21.0173697% of variance in PGSI harm rates.

Calculate Nagelkerke’s R squared for the GHM model:

Show code

NagelkerkeR2_weighted_income_spent_lr_GHM<-NagelkerkeR2(weighted_lr_income_spent_new_limit_GHM) %>%as.data.frame() %>%print() # NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

N R2

1 1055 0.2288529

The model accounts for 22.8852894% of variance in PGSI harm rates.

Risk curve

Plot some risk curves for the relationship between this predictor and the two outcomes.

Show code

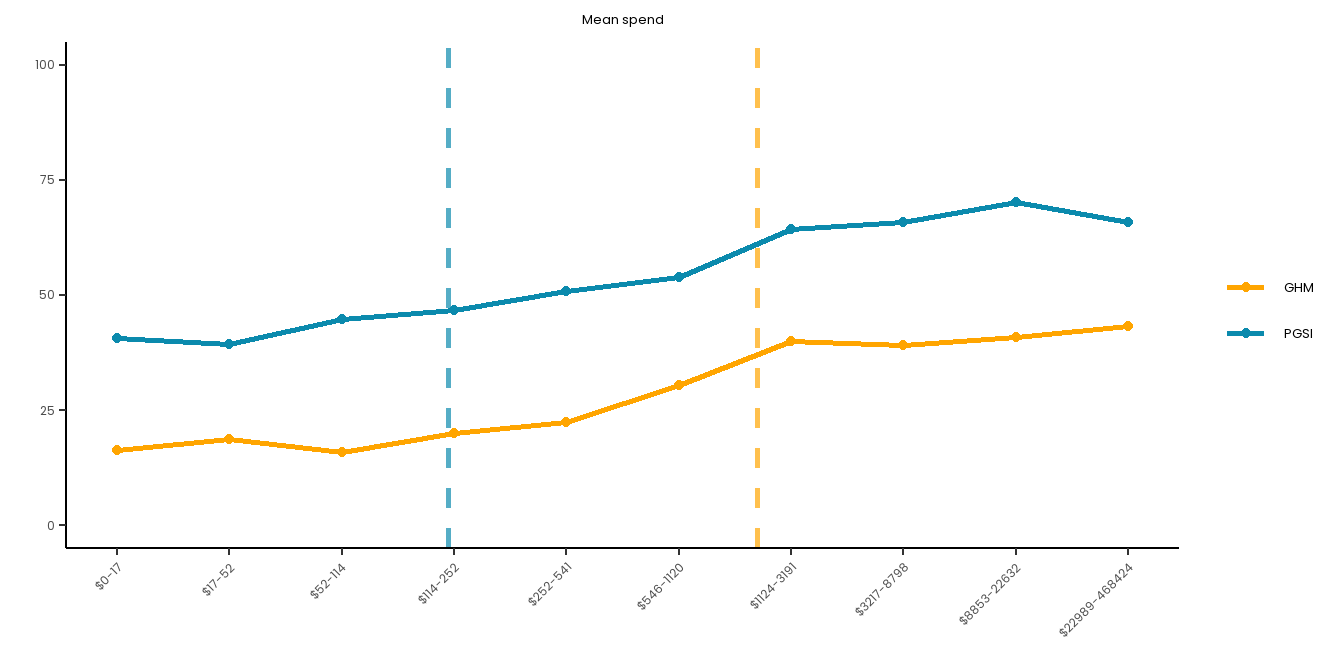

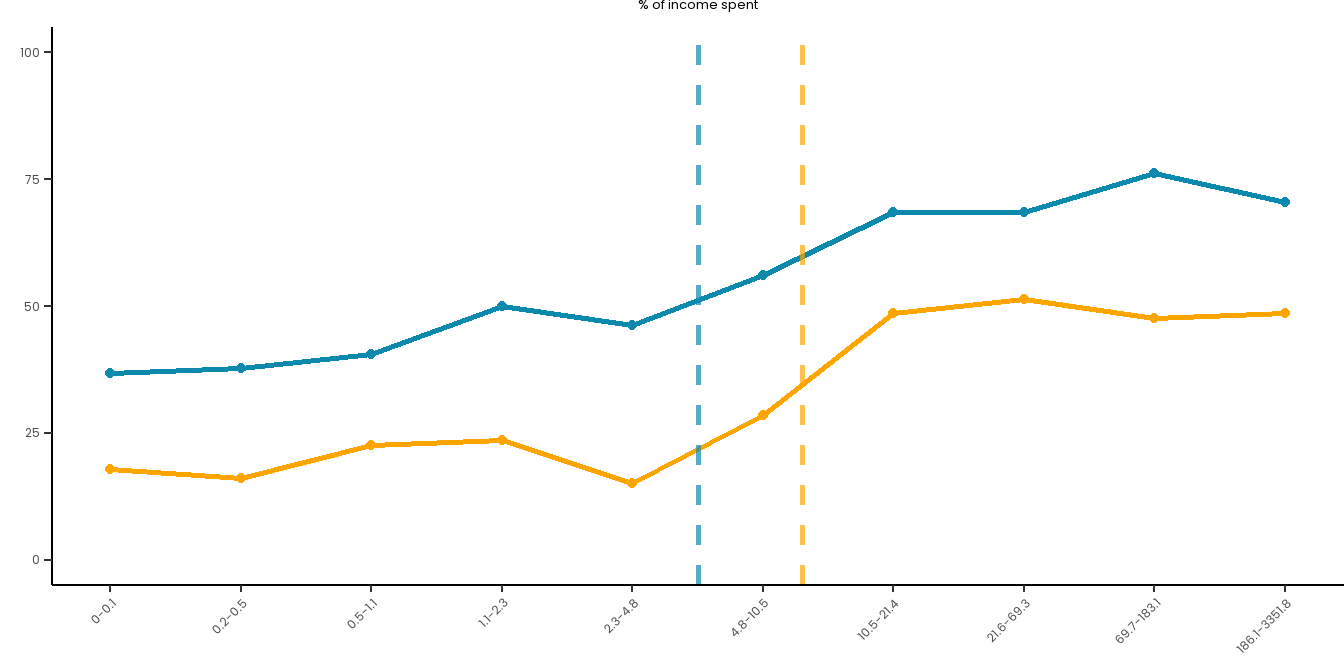

# Create a summary dataset:summary_data <- master_dataset_recoded_w_new_limits %>%mutate(decile =ntile(PERCENT_MON_INCOME_SPENT_MONTHLY_PAS_6M, 10)) %>%group_by(decile) %>%summarise(PGSI_pct =sum(PGSI_STATUS ==1, na.rm =TRUE) /n() *100,GHM_pct =sum(GHM_STATUS ==1, na.rm =TRUE) /n() *100,min_val =min(PERCENT_MON_INCOME_SPENT_MONTHLY_PAS_6M, na.rm =TRUE),max_val =max(PERCENT_MON_INCOME_SPENT_MONTHLY_PAS_6M, na.rm =TRUE) ) %>%mutate(decile_label =paste(round(min_val, 1), round(max_val, 1), sep ="-")) %>%filter(!is.na(decile))long_data <- summary_data %>%pivot_longer(cols =c(PGSI_pct, GHM_pct),names_to ="HarmMeasure",values_to ="pct_harmed" ) %>%mutate(HarmMeasure =case_when(HarmMeasure =="PGSI_pct"~"PGSI", HarmMeasure =="GHM_pct"~"GHM"))# Plot both curves on the same plot for ease:combined_risk_curve_income_spent <-ggplot(long_data, aes(x =as.numeric(decile), y = pct_harmed, color = HarmMeasure, group = HarmMeasure)) +geom_line(size =1) +geom_point() +scale_x_continuous(breaks =1:10, labels = summary_data$decile_label) +labs(title ="% of income spent",x ="",y ="") +ylim(0, 100) +# PGSI LIMIT:geom_vline(xintercept =5.5, linetype ="dashed", color ="#0B8AAD", size =1, alpha =0.7) +# GHM LIMIT:geom_vline(xintercept =6.3, linetype ="dashed", color ="orange", size =1, alpha =0.7) +scale_color_manual(name ="", values =c("PGSI"="#0B8AAD", "GHM"="orange")) + risk_curve_theme +theme(legend.position ="none",plot.margin =margin(0,0,-1,0)) combined_risk_curve_income_spent

tbl_merge(tbls =list(tbl_weighted_lr_n_activities_new_limit_PGSI, tbl_weighted_lr_n_activities_new_limit_GHM),tab_spanner =c("**PGSI Status**", "**GHM Status**")) %>%as_gt() %>%tab_options(data_row.padding =px(1.5)) %>%tab_header(title ="New optimal number of different sport and race types limit for online wagering as a predictor of harm status (demographic-adjusted models)" )

New optimal number of different sport and race types limit for online wagering as a predictor of harm status (demographic-adjusted models)

Characteristic

PGSI Status

GHM Status

OR

95% CI

p-value

OR

95% CI

p-value

AGE

0.97

0.97, 0.98

<0.001

0.97

0.96, 0.98

<0.001

GENDER

Female

—

—

—

—

Male

1.68

1.17, 2.40

0.005

2.25

1.34, 3.78

0.002

Unknown

2.19

0.84, 5.70

0.11

2.36

0.73, 7.64

0.2

EMPLOYMENT_RECODED

Employed

—

—

—

—

Unemployed

1.40

0.78, 2.51

0.3

2.80

1.51, 5.18

0.001

Unknown

1.16

0.87, 1.55

0.3

0.99

0.70, 1.41

>0.9

EDUCATION_NUM

0.90

0.83, 0.97

0.007

0.97

0.89, 1.06

0.5

GAM_ACCOUNTS_NUM

1.34

1.22, 1.48

<0.001

1.33

1.19, 1.47

<0.001

Engages_in_other_forms

FALSE

—

—

—

—

TRUE

1.92

1.40, 2.63

<0.001

1.78

1.22, 2.60

0.003

NEW_LIMIT_PGSI_N_ACTIVITIES

1.55

1.20, 2.00

<0.001

Null deviance

2,283

1,787

Null df

1,646

1,579

AIC

2,096

1,649

BIC

2,147

1,700

Deviance

2,073

1,626

Residual df

1,637

1,570

No. Obs.

1,647

1,580

NEW_LIMIT_GHM_N_ACTIVITIES

1.30

0.95, 1.77

0.10

Abbreviations: CI = Confidence Interval, OR = Odds Ratio

Calculate Nagelkerke’s R squared for the PGSI model:

# NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

The model accounts for 15.9464454% of variance in PGSI harm rates.

Calculate Nagelkerke’s R squared for the GHM model:

Show code

NagelkerkeR2_weighted_n_activities_lr_GHM<-NagelkerkeR2(weighted_lr_n_activities_new_limit_GHM) %>%as.data.frame() %>%print() # NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

N R2

1 1580 0.1425208

The model accounts for 14.2520775% of variance in PGSI harm rates.

Risk Curve

Plot some risk curves for the relationship between this predictor and the two outcomes.

Show code

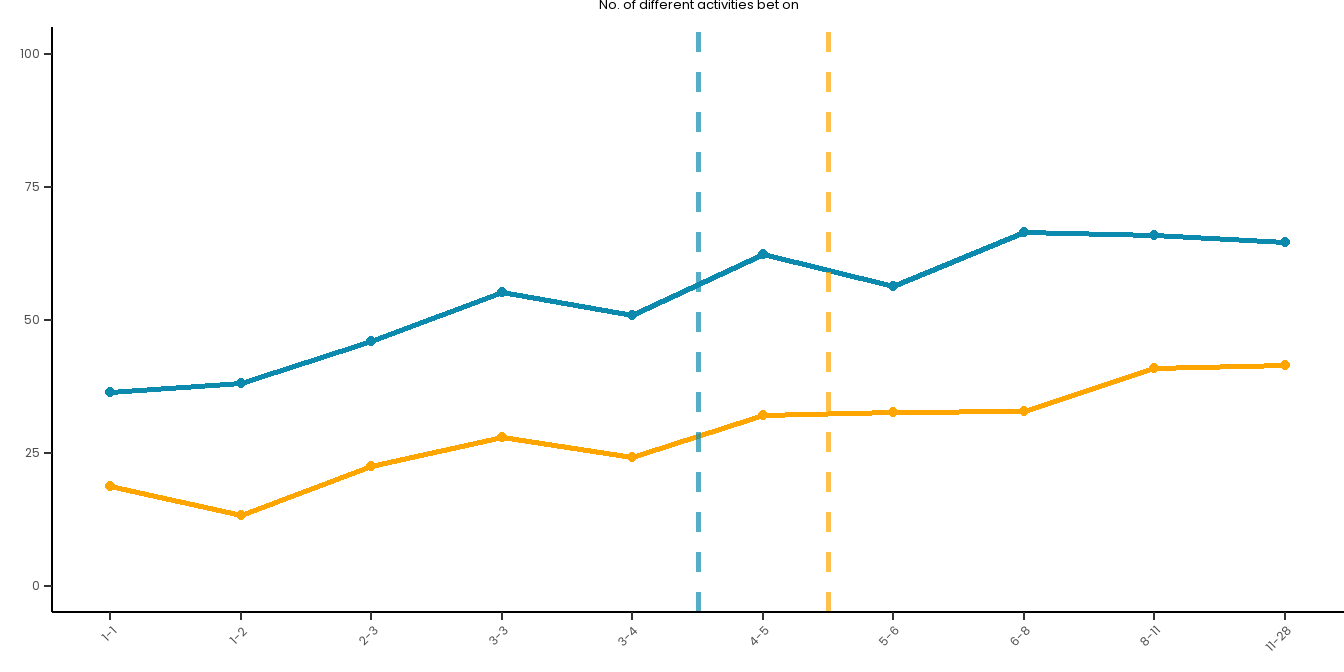

# Create a summary dataset:summary_data <- master_dataset_recoded_w_new_limits %>%mutate(decile =ntile(PAS_6M_N_ACTIVITIES, 10)) %>%group_by(decile) %>%summarise(PGSI_pct =sum(PGSI_STATUS ==1, na.rm =TRUE) /n() *100,GHM_pct =sum(GHM_STATUS ==1, na.rm =TRUE) /n() *100,min_val =min(PAS_6M_N_ACTIVITIES, na.rm =TRUE),max_val =max(PAS_6M_N_ACTIVITIES, na.rm =TRUE) ) %>%mutate(decile_label =paste(round(min_val, 2), round(max_val, 2), sep ="-")) %>%filter(!is.na(decile))long_data <- summary_data %>%pivot_longer(cols =c(PGSI_pct, GHM_pct),names_to ="HarmMeasure",values_to ="pct_harmed" ) %>%mutate(HarmMeasure =case_when(HarmMeasure =="PGSI_pct"~"PGSI", HarmMeasure =="GHM_pct"~"GHM"))# Plot both curves on the same plot for ease:combined_risk_curve_n_activities <-ggplot(long_data, aes(x =as.numeric(decile), y = pct_harmed, color = HarmMeasure, group = HarmMeasure)) +geom_line(size =1) +geom_point() +scale_x_continuous(breaks =1:10, labels = summary_data$decile_label) +labs(title ="No. of different activities bet on",x ="",y ="") +ylim(0, 100) +# PGSI LIMIT:geom_vline(xintercept =5.5, linetype ="dashed", color ="#0B8AAD", size =1, alpha =0.7) +# GHM LIMIT:geom_vline(xintercept =6.5, linetype ="dashed", color ="orange", size =1, alpha =0.7) +scale_color_manual(name ="", values =c("PGSI"="#0B8AAD", "GHM"="orange")) + risk_curve_theme +theme(legend.position ="none",plot.margin =margin(0,0,-1,0)) combined_risk_curve_n_activities

tbl_merge(tbls =list(tbl_weighted_lr_deposit_freq_new_limit_PGSI, tbl_weighted_lr_deposit_freq_new_limit_GHM),tab_spanner =c("**PGSI Status**", "**GHM Status**")) %>%as_gt() %>%tab_options(data_row.padding =px(1.5)) %>%tab_header(title ="New optimal deposit frequency limit for online wagering as a predictor of harm status (demographic-adjusted models)" )

New optimal deposit frequency limit for online wagering as a predictor of harm status (demographic-adjusted models)

Characteristic

PGSI Status

GHM Status

OR

95% CI

p-value

OR

95% CI

p-value

AGE

0.97

0.97, 0.98

<0.001

0.97

0.96, 0.98

<0.001

GENDER

Female

—

—

—

—

Male

1.60

1.11, 2.29

0.011

2.12

1.27, 3.54

0.004

Unknown

2.02

0.72, 5.67

0.2

1.74

0.49, 6.19

0.4

EMPLOYMENT_RECODED

Employed

—

—

—

—

Unemployed

1.38

0.76, 2.50

0.3

2.63

1.45, 4.79

0.002

Unknown

1.06

0.79, 1.43

0.7

0.90

0.62, 1.31

0.6

EDUCATION_NUM

0.91

0.84, 0.98

0.015

0.98

0.89, 1.07

0.6

GAM_ACCOUNTS_NUM

1.36

1.24, 1.50

<0.001

1.37

1.23, 1.53

<0.001

Engages_in_other_forms

FALSE

—

—

—

—

TRUE

1.94

1.41, 2.66

<0.001

1.75

1.19, 2.56

0.004

NEW_LIMIT_PGSI_DEPOSIT_FREQ

2.60

2.01, 3.36

<0.001

Null deviance

2,283

1,787

Null df

1,646

1,579

AIC

2,041

1,590

BIC

2,091

1,641

Deviance

2,017

1,567

Residual df

1,637

1,570

No. Obs.

1,647

1,580

NEW_LIMIT_GHM_DEPOSIT_FREQ

3.39

2.42, 4.75

<0.001

Abbreviations: CI = Confidence Interval, OR = Odds Ratio

Calculate Nagelkerke’s R squared for the PGSI model:

# NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

The model accounts for 19.8684028% of variance in PGSI harm rates.

Calculate Nagelkerke’s R squared for the GHM model:

Show code

NagelkerkeR2_weighted_deposit_freq_lr_GHM<-NagelkerkeR2(weighted_lr_deposit_freq_new_limit_GHM) %>%as.data.frame() %>%print() # NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

N R2

1 1580 0.1915685

The model accounts for 19.1568532% of variance in PGSI harm rates.

Risk Curve

Plot some risk curves for the relationship between this predictor and the two outcomes.

# NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

The model accounts for 19.0144593% of variance in PGSI harm rates.

Calculate Nagelkerke’s R squared for the GHM model:

Show code

NagelkerkeR2_weighted_deposit_amount_lr_GHM<-NagelkerkeR2(weighted_lr_deposit_amount_new_limit_GHM) %>%as.data.frame() %>%print() # NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

N R2

1 1580 0.1824433

The model accounts for 18.2443336% of variance in PGSI harm rates.

Risk curve

Plot some risk curves for the relationship between this predictor and the two outcomes.

tbl_merge(tbls =list(tbl_weighted_lr_income_deposited_new_limit_PGSI, tbl_weighted_lr_income_deposited_new_limit_GHM),tab_spanner =c("**PGSI Status**", "**GHM Status**")) %>%as_gt() %>%tab_options(data_row.padding =px(1.5)) %>%tab_header(title ="New optimal amount of income deposited limit for online wagering as a predictor of harm status (demographic-adjusted models)" )

New optimal amount of income deposited limit for online wagering as a predictor of harm status (demographic-adjusted models)

Characteristic

PGSI Status

GHM Status

OR

95% CI

p-value

OR

95% CI

p-value

AGE

0.97

0.96, 0.98

<0.001

0.97

0.96, 0.98

<0.001

GENDER

Female

—

—

—

—

Male

1.71

1.06, 2.76

0.028

2.53

1.28, 4.97

0.007

Unknown

3.53

0.92, 13.6

0.067

2.09

0.32, 13.8

0.4

EMPLOYMENT_RECODED

Employed

—

—

—

—

Unemployed

1.06

0.52, 2.17

0.9

1.92

0.84, 4.38

0.12

EDUCATION_NUM

0.91

0.84, 1.00

0.045

0.96

0.87, 1.06

0.4

GAM_ACCOUNTS_NUM

1.35

1.20, 1.52

<0.001

1.40

1.23, 1.60

<0.001

Engages_in_other_forms

FALSE

—

—

—

—

TRUE

2.15

1.44, 3.19

<0.001

1.96

1.20, 3.18

0.007

NEW_LIMIT_PGSI_INCOME_DEPOSITED

3.78

2.70, 5.30

<0.001

Null deviance

1,527

1,288

Null df

1,054

1,054

AIC

1,330

1,122

BIC

1,373

1,164

Deviance

1,310

1,101

Residual df

1,046

1,046

No. Obs.

1,055

1,055

NEW_LIMIT_GHM_INCOME_DEPOSITED

7.10

4.50, 11.2

<0.001

Abbreviations: CI = Confidence Interval, OR = Odds Ratio

Calculate Nagelkerke’s R squared for the PGSI model:

# NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

The model accounts for 24.2618149% of variance in PGSI harm rates.

Calculate Nagelkerke’s R squared for the GHM model:

Show code

NagelkerkeR2_weighted_income_deposited_lr_GHM<-NagelkerkeR2(weighted_lr_income_deposited_new_limit_GHM) %>%as.data.frame() %>%print() # NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

N R2

1 1055 0.2307804

The model accounts for 23.0780376% of variance in PGSI harm rates.

Risk curve

Plot some risk curves for the relationship between this predictor and the two outcomes.

Show code

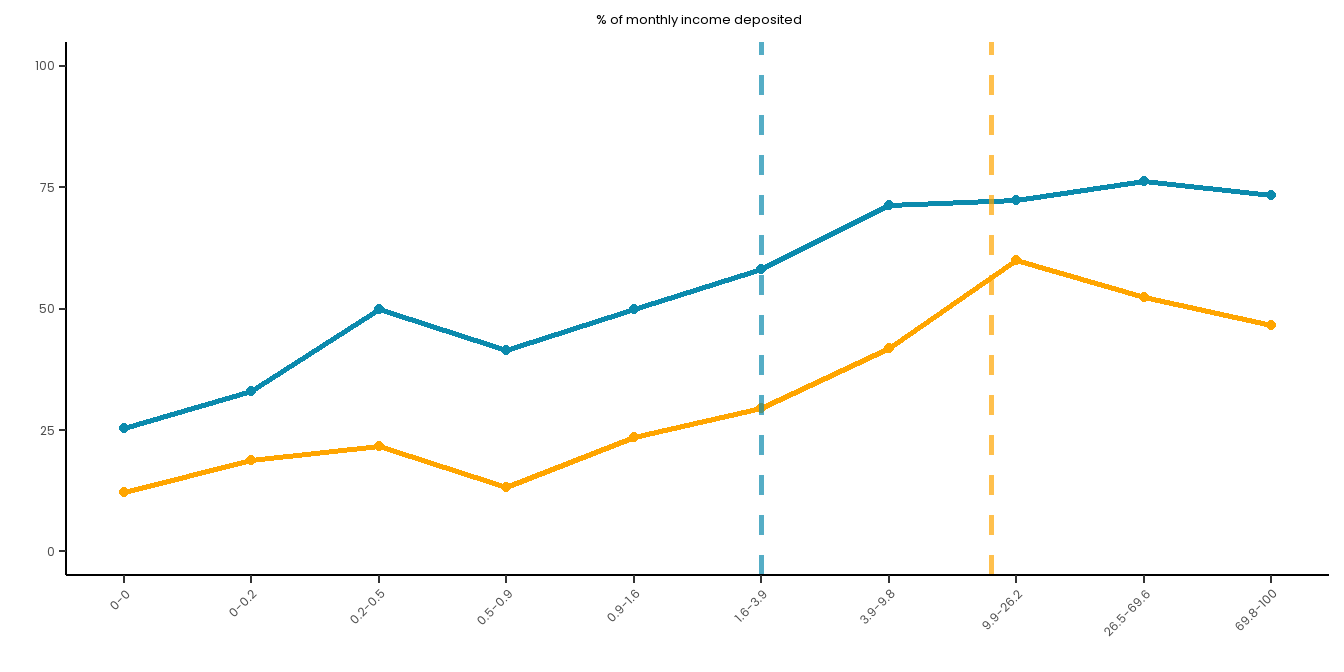

# Create a summary dataset:summary_data <- master_dataset_recoded_w_new_limits %>%mutate(decile =ntile(PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M, 10)) %>%group_by(decile) %>%summarise(PGSI_pct =sum(PGSI_STATUS ==1, na.rm =TRUE) /n() *100,GHM_pct =sum(GHM_STATUS ==1, na.rm =TRUE) /n() *100,min_val =min(PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M, na.rm =TRUE),max_val =max(PERCENT_MON_INCOME_DEPOSIT_MONTHLY_PAS_6M, na.rm =TRUE) ) %>%mutate(decile_label =paste(round(min_val, 1), round(max_val, 1), sep ="-")) %>%filter(!is.na(decile))long_data <- summary_data %>%pivot_longer(cols =c(PGSI_pct, GHM_pct),names_to ="HarmMeasure",values_to ="pct_harmed" ) %>%mutate(HarmMeasure =case_when(HarmMeasure =="PGSI_pct"~"PGSI", HarmMeasure =="GHM_pct"~"GHM"))# Plot both curves on the same plot for ease:combined_risk_curve_income_deposited<-ggplot(long_data, aes(x =as.numeric(decile), y = pct_harmed, color = HarmMeasure, group = HarmMeasure)) +geom_line(size =1) +geom_point() +scale_x_continuous(breaks =1:10, labels = summary_data$decile_label) +labs(title ="% of monthly income deposited",x ="",y ="") +ylim(0, 100) + risk_curve_theme +# PGSI LIMIT:geom_vline(xintercept =6, linetype ="dashed", color ="#0B8AAD", size =1, alpha =0.7) +# GHM LIMIT:geom_vline(xintercept =7.8, linetype ="dashed", color ="orange", size =1, alpha =0.7) +scale_color_manual(name ="", values =c("PGSI"="#0B8AAD", "GHM"="orange")) +theme(legend.position ="none")combined_risk_curve_income_deposited

tbl_merge(tbls =list(tbl_weighted_lr_gam_accounts_new_limit_PGSI, tbl_weighted_lr_gam_accounts_new_limit_GHM),tab_spanner =c("**PGSI Status**", "**GHM Status**")) %>%as_gt() %>%tab_options(data_row.padding =px(1.5)) %>%tab_header(title ="New optimal number of wagering accounts limit for online wagering as a predictor of harm status (demographic-adjusted models)" )

New optimal number of wagering accounts limit for online wagering as a predictor of harm status (demographic-adjusted models)

Characteristic

PGSI Status

GHM Status

OR

95% CI

p-value

OR

95% CI

p-value

AGE

0.97

0.96, 0.98

<0.001

0.97

0.96, 0.98

<0.001

GENDER

Female

—

—

—

—

Male

1.82

1.27, 2.61

0.001

2.62

1.57, 4.38

<0.001

Unknown

2.51

0.98, 6.39

0.054

2.96

0.91, 9.57

0.070

EMPLOYMENT_RECODED

Employed

—

—

—

—

Unemployed

1.36

0.77, 2.39

0.3

2.74

1.49, 5.05

0.001

Unknown

1.16

0.87, 1.54

0.3

0.96

0.68, 1.36

0.8

EDUCATION_NUM

0.90

0.83, 0.97

0.007

0.97

0.89, 1.06

0.5

Engages_in_other_forms

FALSE

—

—

—

—

TRUE

1.88

1.38, 2.57

<0.001

1.77

1.22, 2.57

0.003

NEW_LIMIT_PGSI_GAM_ACCOUNTS

2.17

1.71, 2.76

<0.001

Null deviance

2,283

1,787

Null df

1,646

1,579

AIC

2,108

1,665

BIC

2,154

1,711

Deviance

2,087

1,645

Residual df

1,638

1,571

No. Obs.

1,647

1,580

NEW_LIMIT_GHM_GAM_ACCOUNTS

1.83

1.38, 2.44

<0.001

Abbreviations: CI = Confidence Interval, OR = Odds Ratio

Calculate Nagelkerke’s R squared for the PGSI model:

# NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

The model accounts for 14.9389916% of variance in PGSI harm rates.

Calculate Nagelkerke’s R squared for the GHM model:

Show code

NagelkerkeR2_weighted_gam_accounts_lr_GHM<-NagelkerkeR2(weighted_lr_gam_accounts_new_limit_GHM) %>%as.data.frame() %>%print() # NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

N R2

1 1580 0.1266771

The model accounts for 12.6677066% of variance in PGSI harm rates.

Risk curve

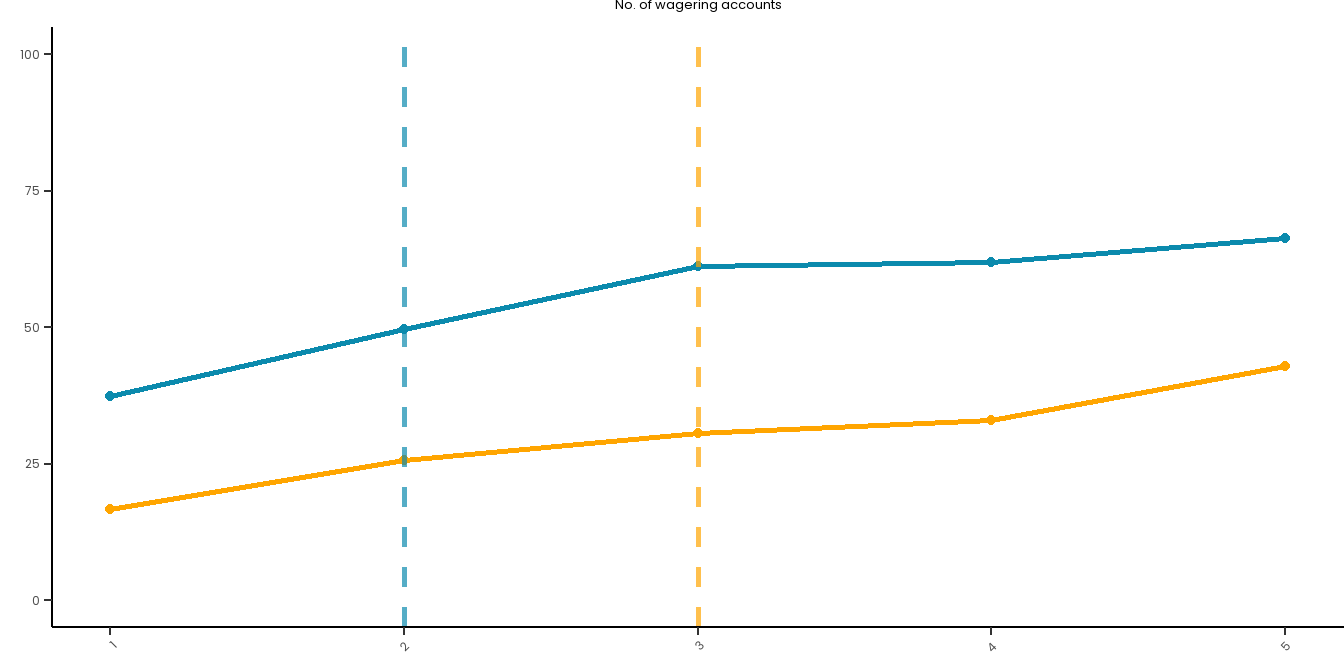

Plot some risk curves for the relationship between this predictor and the two outcomes. We won’t use deciles here as the values are so low in range:

Show code

# Create a summary dataset:summary_data <- master_dataset_recoded_w_new_limits %>%group_by(GAM_ACCOUNTS_NUM) %>%summarise(PGSI_pct =sum(PGSI_STATUS ==1, na.rm =TRUE) /n() *100,GHM_pct =sum(GHM_STATUS ==1, na.rm =TRUE) /n() *100 ) long_data <- summary_data %>%pivot_longer(cols =c(PGSI_pct, GHM_pct),names_to ="HarmMeasure",values_to ="pct_harmed" ) %>%mutate(HarmMeasure =case_when(HarmMeasure =="PGSI_pct"~"PGSI", HarmMeasure =="GHM_pct"~"GHM"))# Plot both curves on the same plot for ease:combined_risk_curve_n_accounts<-ggplot(long_data, aes(x = GAM_ACCOUNTS_NUM, y = pct_harmed,color = HarmMeasure, group = HarmMeasure)) +geom_line(size =1) +geom_point() +ylim(0, 100) +scale_x_continuous(breaks =1:5) +labs(title ="No. of wagering accounts", x ="",y ="") +# PGSI LIMIT:geom_vline(xintercept =2, linetype ="dashed", color ="#0B8AAD", size =1, alpha =0.7) +# GHM LIMIT:geom_vline(xintercept =3, linetype ="dashed", color ="orange", size =1, alpha =0.7) +scale_color_manual(name ="", values =c("PGSI"="#0B8AAD", "GHM"="orange")) + risk_curve_theme +theme(legend.position ="none",plot.margin =margin(0,0,-1,0)) combined_risk_curve_n_accounts

All-limit adjusted model

And now perform the models that incorporate all of the new limits to determine the independent predictive ability of each limit:

tbl_merge(tbls =list(tbl_weighted_lr_all_limit_PGSI, tbl_weighted_lr_all_limit_GHM),tab_spanner =c("**PGSI Status**", "**GHM Status**")) %>%as_gt() %>%tab_options(data_row.padding =px(1.5)) %>%tab_header(title ="New optimal limits for online wagering as a predictor of harm status (demographic- and limit-adjusted models)" )

New optimal limits for online wagering as a predictor of harm status (demographic- and limit-adjusted models)

Characteristic

PGSI Status

GHM Status

OR

95% CI

p-value

OR

95% CI

p-value

AGE

0.98

0.96, 0.99

<0.001

0.97

0.96, 0.99

<0.001

GENDER

Female

—

—

—

—

Male

1.65

1.01, 2.71

0.047

2.64

1.32, 5.26

0.006

Unknown

3.01

0.83, 10.9

0.094

2.18

0.45, 10.7

0.3

EMPLOYMENT_RECODED

Employed

—

—

—

—

Unemployed

1.16

0.55, 2.43

0.7

1.58

0.72, 3.44

0.3

EDUCATION_NUM

0.93

0.85, 1.02

0.12

0.99

0.90, 1.10

>0.9

Engages_in_other_forms

FALSE

—

—

—

—

TRUE

2.22

1.46, 3.36

<0.001

2.11

1.29, 3.45

0.003

NEW_LIMIT_PGSI_BET_FREQ

0.36

0.22, 0.60

<0.001

NEW_LIMIT_PGSI_SPEND

1.18

0.68, 2.04

0.6

NEW_LIMIT_PGSI_INCOME_SPENT

1.23

0.68, 2.22

0.5

NEW_LIMIT_PGSI_N_ACTIVITIES

1.25

0.87, 1.81

0.2

NEW_LIMIT_PGSI_DEPOSIT_FREQ

2.25

1.36, 3.73

0.002

NEW_LIMIT_PGSI_DEPOSIT_AMOUNT

1.48

0.91, 2.40

0.12

NEW_LIMIT_PGSI_INCOME_DEPOSITED

2.21

1.25, 3.90

0.007

NEW_LIMIT_PGSI_GAM_ACCOUNTS

1.94

1.41, 2.65

<0.001

Null deviance

1,527

1,288

Null df

1,054

1,054

AIC

1,311

1,100

BIC

1,379

1,168

Deviance

1,274

1,063

Residual df

1,040

1,040

No. Obs.

1,055

1,055

NEW_LIMIT_GHM_BET_FREQ

0.27

0.14, 0.51

<0.001

NEW_LIMIT_GHM_SPEND

1.31

0.57, 3.01

0.5

NEW_LIMIT_GHM_INCOME_SPENT

3.50

1.94, 6.34

<0.001

NEW_LIMIT_GHM_N_ACTIVITIES

0.92

0.59, 1.43

0.7

NEW_LIMIT_GHM_DEPOSIT_FREQ

3.12

1.63, 5.98

<0.001

NEW_LIMIT_GHM_DEPOSIT_AMOUNT

0.63

0.25, 1.55

0.3

NEW_LIMIT_GHM_INCOME_DEPOSITED

3.22

1.48, 6.98

0.003

NEW_LIMIT_GHM_GAM_ACCOUNTS

2.04

1.42, 2.95

<0.001

Abbreviations: CI = Confidence Interval, OR = Odds Ratio

Calculate Nagelkerke’s R squared for the PGSI model:

# NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

The model accounts for 27.8025472% of variance in PGSI harm rates.

Calculate Nagelkerke’s R squared for the GHM model:

Show code

NagelkerkeR2_weighted_all_limit_lr_GHM<-NagelkerkeR2(weighted_lr_all_limit_GHM) %>%as.data.frame() %>%print() # NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

N R2

1 1055 0.2724964

The model accounts for 27.2496388% of variance in PGSI harm rates.

Show code

# First, extract the model coefficients:model_coefs <-coef(weighted_lr_all_limit_PGSI)# Define the NEW_LIMIT variables in the order you want to accumulate them.# (Change the order below if you wish to follow a different sequence.)new_limit_vars <-c( "NEW_LIMIT_PGSI_DEPOSIT_FREQ","NEW_LIMIT_PGSI_INCOME_DEPOSITED","NEW_LIMIT_PGSI_GAM_ACCOUNTS")# Extract the intercept (baseline for a reference person, with demographics at reference)baseline <- model_coefs["(Intercept)"]# Initialize a vector to store the cumulative linear predictors (z)cumulative_z <-numeric(length(new_limit_vars))# And a vector to store probabilitiescumulative_prob <-numeric(length(new_limit_vars))# Loop through the NEW_LIMIT variables in the specified orderfor(i inseq_along(new_limit_vars)) {# For the cumulative effect, add the coefficient for the current indicator.# For the first indicator, add it to the intercept;# for subsequent ones, add the new coefficient to the previous cumulative sum.if(i ==1) { cumulative_z[i] <- baseline + model_coefs[new_limit_vars[i]] } else { cumulative_z[i] <- cumulative_z[i -1] + model_coefs[new_limit_vars[i]] }# Compute the predicted probability using the logistic function: cumulative_prob[i] <-exp(cumulative_z[i]) / (1+exp(cumulative_z[i]))}# Create a summary table:cumulative_summary <-data.frame("Number_of_Indicators"=1:length(new_limit_vars),"Cumulative_z"=round(cumulative_z, 3),"Predicted_Probability"=round(cumulative_prob, 3),"Predicted_Probability_Percent"=round(cumulative_prob *100, 1))print(cumulative_summary)

Finally, the test H3, we need to look at how the accumulation of limits past relates to harm. From our preregistration:

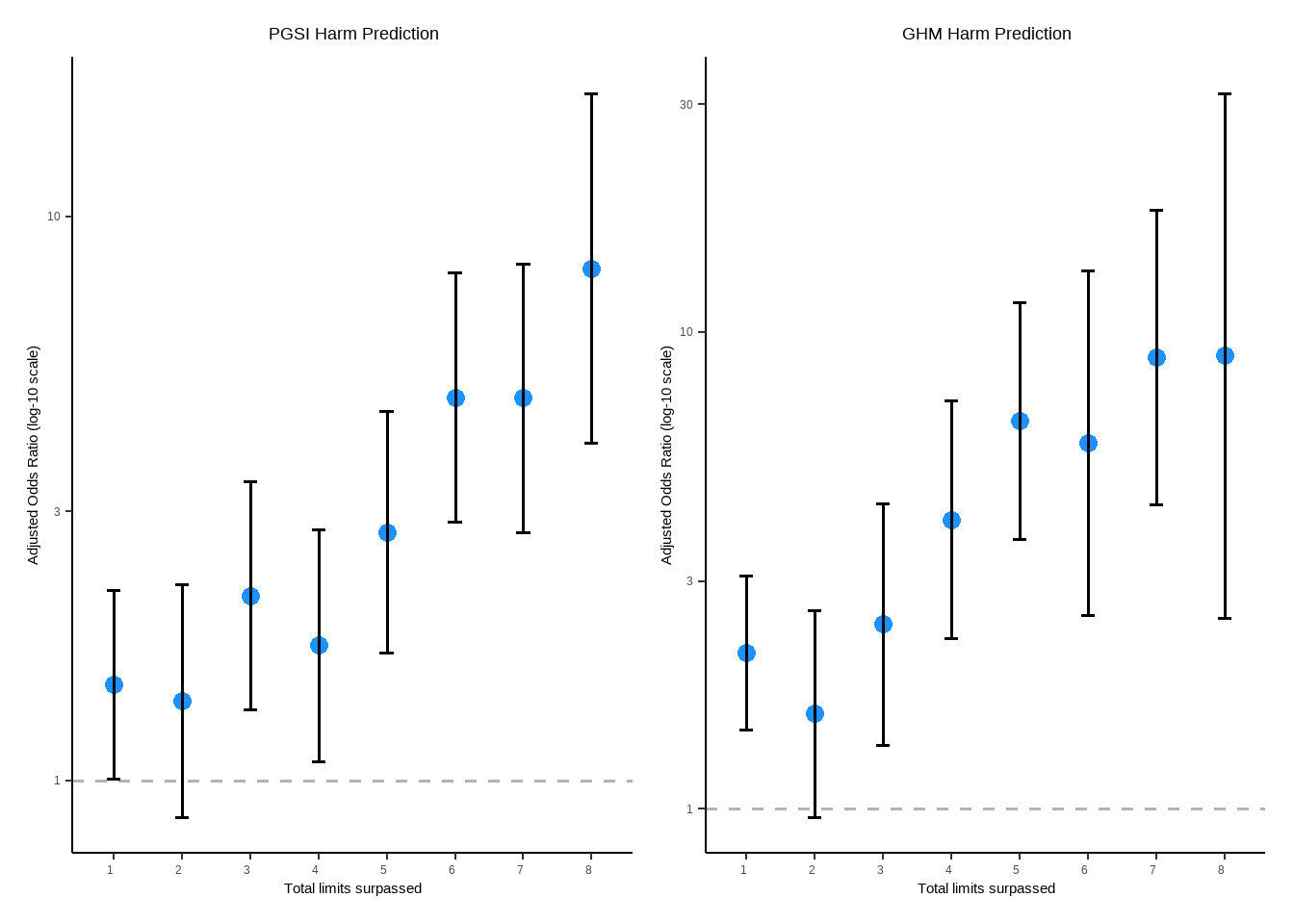

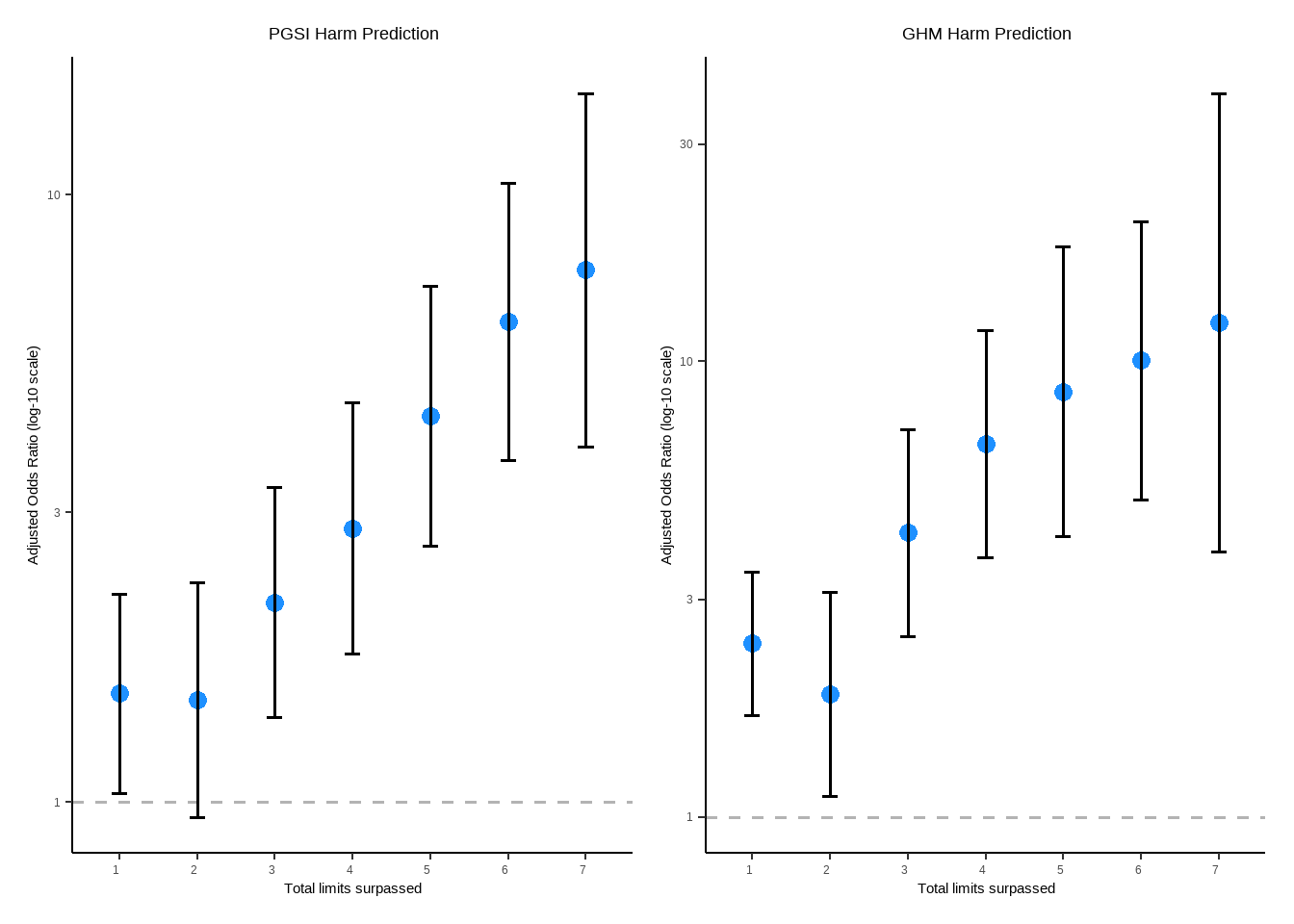

H3: Participants who surpass successively more of the eight newly derived low-risk in the six months preceding survey participation will have an increasingly greater odds of reporting the experience of harm after accounting for the impact of demographic factors (i.e., age, gender, employment status, and education level) on harm. That is, using logistic regression models with harm status as the outcome and the number of limits passed as an ordered categorical predictor variable, there will be a monotonic relationship between the number of limits passed and odds of harm (i.e., a larger odds ratio with each additional limit passed). [Limit evaluation: cumulative impact of limit breaches on harm status]

tbl_merge(tbls =list(tbl_weighted_lr_limit_count_PGSI, tbl_weighted_lr_limit_count_GHM),tab_spanner =c("**PGSI Status**", "**GHM Status**")) %>%as_gt() %>%tab_options(data_row.padding =px(1.5)) %>%tab_header(title ="Cumulative number of limits passed as a predictor of harm status (demographic-adjusted models)" )

Cumulative number of limits passed as a predictor of harm status (demographic-adjusted models)

Characteristic

PGSI Status

GHM Status

OR

95% CI

p-value

OR

95% CI

p-value

AGE

0.97

0.96, 0.98

<0.001

0.97

0.96, 0.98

<0.001

GENDER

Female

—

—

—

—

Male

1.71

1.19, 2.44

0.003

2.06

1.23, 3.47

0.006

Unknown

2.42

0.82, 7.17

0.11

2.03

0.56, 7.37

0.3

EMPLOYMENT_RECODED

Employed

—

—

—

—

Unemployed

1.37

0.74, 2.54

0.3

2.50

1.32, 4.72

0.005

Unknown

1.28

0.95, 1.71

0.10

0.96

0.66, 1.39

0.8

EDUCATION_NUM

0.92

0.85, 0.99

0.035

0.99

0.90, 1.08

0.8

Engages_in_other_forms

FALSE

—

—

—

—

TRUE

2.06

1.49, 2.85

<0.001

1.92

1.30, 2.82

<0.001

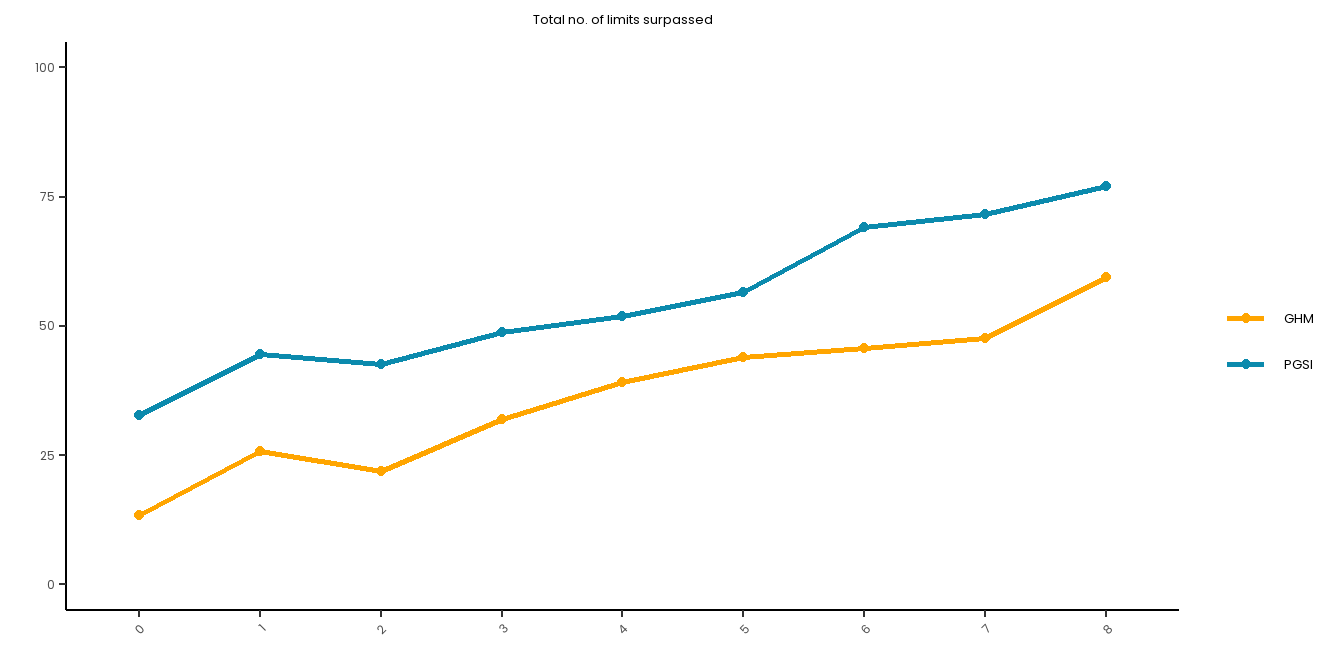

TOTAL_LIMITS_REACHED_PGSI

0

—

—

1

1.48

1.01, 2.18

0.046

2

1.39

0.86, 2.23

0.2

3

2.13

1.33, 3.39

0.002

4

1.74

1.08, 2.79

0.022

5

2.76

1.68, 4.52

<0.001

6

4.78

2.87, 7.97

<0.001

7

4.77

2.76, 8.24

<0.001

8

8.09

3.96, 16.5

<0.001

Null deviance

2,283

1,787

Null df

1,646

1,579

AIC

2,068

1,599

BIC

2,147

1,680

Deviance

2,029

1,562

Residual df

1,631

1,564

No. Obs.

1,647

1,580

TOTAL_LIMITS_REACHED_GHM

0

—

—

1

2.12

1.46, 3.08

<0.001

2

1.58

0.96, 2.60

0.071

3

2.44

1.36, 4.37

0.003

4

4.04

2.27, 7.16

<0.001

5

6.51

3.67, 11.6

<0.001

6

5.84

2.54, 13.4

<0.001

7

8.85

4.35, 18.0

<0.001

8

8.92

2.52, 31.7

<0.001

Abbreviations: CI = Confidence Interval, OR = Odds Ratio

Exponentiate coefficients and interpret them as odds-ratios in a data frame:

Show code

sumarisedORs_weighted_lr_limit_count_PGSI<-exp(cbind(OR =coef(weighted_lr_limit_count_PGSI), confint(weighted_lr_limit_count_PGSI)))sumarisedORs_weighted_lr_limit_count_PGSI %>%as.data.frame() %>%rownames_to_column() %>%mutate(across(c(OR, `2.5 %`, `97.5 %`), ~round(., 4))) %>%filter(str_detect(rowname, "TOTAL")) %>%mutate(rowname =str_remove(rowname, "TOTAL_LIMITS_REACHED_PGSI")) %>%gt() %>%tab_options(data_row.padding =px(1.5)) %>%tab_header(md("**Odds ratios with 95% CIs: Total number of limits passed (PGSI)**"), subtitle =NULL) %>%cols_label('2.5 %'="Lower CI: 2.5%",'97.5 %'="Upper CI: 97.5%")

Odds ratios with 95% CIs: Total number of limits passed (PGSI)

OR

Lower CI: 2.5%

Upper CI: 97.5%

1

1.4815

1.0077

2.1781

2

1.3868

0.8621

2.2309

3

2.1277

1.3338

3.3942

4

1.7375

1.0830

2.7876

5

2.7577

1.6837

4.5167

6

4.7812

2.8700

7.9652

7

4.7652

2.7551

8.2420

8

8.0913

3.9599

16.5330

Show code

sumarisedORs_weighted_lr_limit_count_GHM<-exp(cbind(OR =coef(weighted_lr_limit_count_GHM), confint(weighted_lr_limit_count_GHM)))sumarisedORs_weighted_lr_limit_count_GHM %>%as.data.frame() %>%rownames_to_column() %>%mutate(across(c(OR, `2.5 %`, `97.5 %`), ~round(., 4))) %>%filter(str_detect(rowname, "TOTAL")) %>%mutate(rowname =str_remove(rowname, "TOTAL_LIMITS_REACHED_GHM")) %>%gt() %>%tab_options(data_row.padding =px(1.5)) %>%tab_header(md("**Odds ratios with 95% CIs: Total number of limits passed (GHM)**"), subtitle =NULL) %>%cols_label('2.5 %'="Lower CI: 2.5%",'97.5 %'="Upper CI: 97.5%")

Odds ratios with 95% CIs: Total number of limits passed (GHM)

# NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

The model accounts for 19.0837288% of variance in PGSI harm rates.

Calculate Nagelkerke’s R squared for the GHM model:

Show code

NagelkerkeR2_weighted_lr_limit_count_PGSI<-NagelkerkeR2(weighted_lr_limit_count_GHM) %>%as.data.frame() %>%print() # NOTE: R2 is calculate as a proportion here and so in the paper we have multiplied it by 100 to form a percentage value

N R2

1 1580 0.1954103

The model accounts for 19.5410337% of variance in GHM harm rates.

tbl_merge(tbls =list(tbl_weighted_lr_limit_count_sans_freq_PGSI, tbl_weighted_lr_limit_count_sans_freq_GHM),tab_spanner =c("**PGSI Status**", "**GHM Status**")) %>%as_gt() %>%tab_options(data_row.padding =px(1.5)) %>%tab_header(title ="Cumulative number of limits passed as a predictor of harm status (demographic-adjusted models)" )

Cumulative number of limits passed as a predictor of harm status (demographic-adjusted models)

Characteristic

PGSI Status

GHM Status

OR

95% CI

p-value

OR

95% CI

p-value

AGE

0.97

0.96, 0.98

<0.001

0.97

0.96, 0.98

<0.001

GENDER

Female

—

—

—

—

Male

1.63

1.14, 2.33

0.008

1.99

1.18, 3.36

0.010

Unknown

2.22